Finastra

Founded Year

2017Stage

Line of Credit | AliveTotal Raised

$5.3BLast Raised

$500M | 1 yr agoMosaic Score The Mosaic Score is an algorithm that measures the overall financial health and market potential of private companies.

+38 points in the past 30 days

About Finastra

Finastra provides a range of financial services, treasury, lending, and banking software solutions. The company offers a wide range of services including lending and corporate banking, payments, treasury and capital markets, universal banking, and investment management. It primarily serves the financial technology industry. It was founded in 2017 and is based in London, United Kingdom.

Loading...

ESPs containing Finastra

The ESP matrix leverages data and analyst insight to identify and rank leading companies in a given technology landscape.

The cloud-based core banking solutions market offers financial institutions the opportunity to modernize outdated legacy systems and provide customers with personalized products and services. The market is competitive, with vendors offering cloud-native solutions that are scalable, secure, and cost-effective. The use of APIs and microservices architecture allows for quick integration with other sy…

Finastra named as Outperformer among 15 other companies, including Temenos, Oracle, and FIS.

Loading...

Research containing Finastra

Get data-driven expert analysis from the CB Insights Intelligence Unit.

CB Insights Intelligence Analysts have mentioned Finastra in 5 CB Insights research briefs, most recently on Aug 23, 2024.

Aug 23, 2024

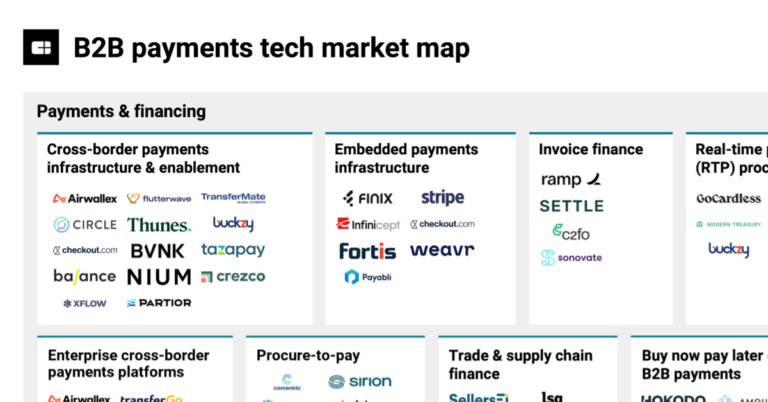

The B2B payments tech market map

May 8, 2024

The embedded banking & payments market map

Mar 14, 2024

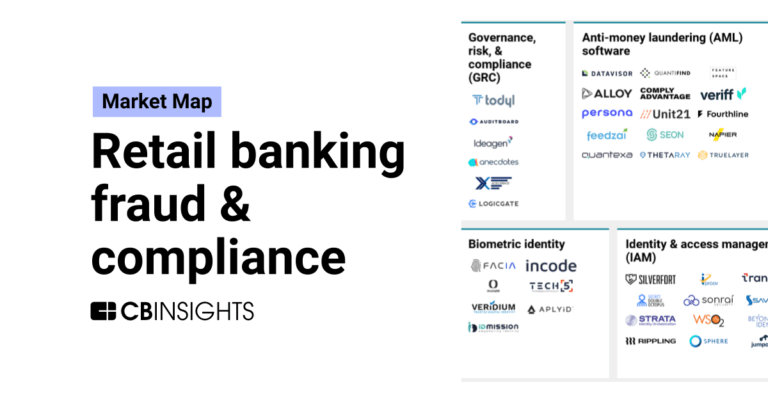

The retail banking fraud & compliance market map

Jan 4, 2024

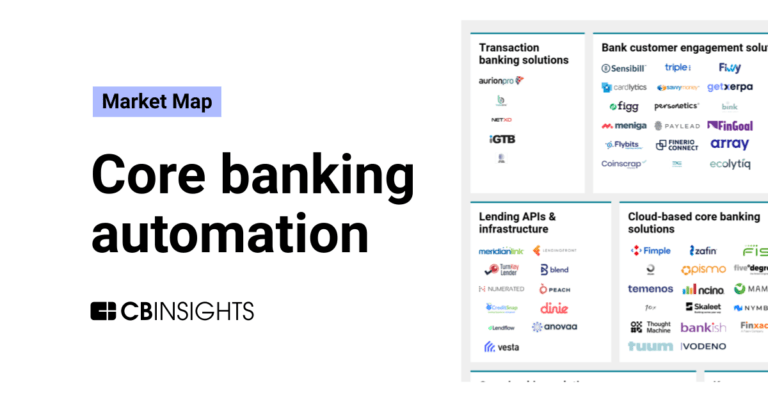

The core banking automation market map

Oct 26, 2023

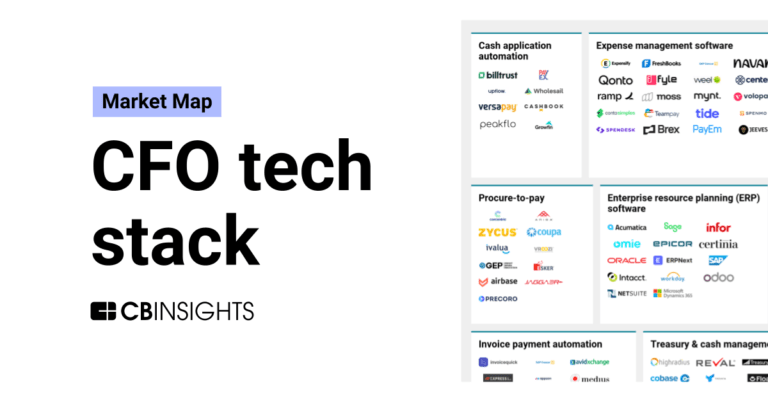

The CFO tech stack market mapExpert Collections containing Finastra

Expert Collections are analyst-curated lists that highlight the companies you need to know in the most important technology spaces.

Finastra is included in 4 Expert Collections, including Digital Lending.

Digital Lending

2,271 items

This collection contains companies that provide alternative means for obtaining a loan for personal or business use and companies that provide software to lenders for the application, underwriting, funding or loan collection process.

Fintech

13,413 items

Excludes US-based companies

Digital Banking

871 items

ITC Vegas 2024 - Exhibitors and Sponsors

699 items

Created 9/9/24. Updated 10.22.24. Company list source: ITC Vegas. Check ITC Vegas' website for final list: https://events.clarionevents.com/InsureTech2024/Public/EventMap.aspx?shMode=E&ID=84001

Latest Finastra News

Oct 24, 2024

25th October 2024 The financial services sector is transitioning to a more open environment, by leveraging the power of connected ecosystems, shared data and platform-based innovation. In this article, industry leaders Simon Paris, CEO of Finastra , and Bill Borden, corporate vice president, worldwide financial services, Microsoft, discuss how the market can collaborate to build new financial ecosystems for growth, encourage sustainable practices and decision-making, and drive positive societal change to empower more people, businesses and communities. Simon Paris: “At Finastra, we’ve always believed that the collective adoption of Open Finance could result in something truly transformative for the industry, and the world. Recently, we identified three major outcomes of Open Finance: firstly, it creates entire new financial ecosystems; secondly, it can underpin more sustainable decisions; and thirdly, it can drive positive societal change and bring more people, businesses and communities into financial wellness. But let’s start with the macroeconomic view; what do you see at that level that is either driving, or hindering, Open Finance?” Bill Borden, Microsoft (Image source: Microsoft) Bill Borden: “There are a lot of macro forces at play right now. One is the cost of capital – a zero cost drove a lot of investment to fintechs over the last decade, and they were pushing the model around what traditional finance truly meant. Second was the involvement of governments and regulators, which drove Open Banking. And third was the democratisation of technology; rising consumer expectations drove institutions to rethink products and services, and how those could be integrated into the customer experience. They’re the big factors going on around the world, albeit at different paces.” Simon: “This explosion of fintechs started around 11 or 12 years ago, but there was initially hesitation from the financial institutions, wondering if it was an opportunity or a threat. Would you say it’s stabilising?” Bill: “Yes, we saw institutions ask themselves, if the smaller organisations can offer these capabilities, why can’t we? We mapped an XY axis, with X representing how they were building and modernising their tech stack to directly interface with customers, and the Y being how to extend out into user journeys and compete with fintechs. Then the question moved to, do we build it out ourselves, do we partner, or do we buy? We’ve seen that mature a lot over the last few years.” Simon: “I love the XY analogy. We took a similar approach at Finastra ; expanding and industrialising our mission-critical software, but consuming capabilities that aren’t our core competencies, like biometric authentication or Generative AI. And that leads into our first outcome of Open Finance: creating new ecosystems. What’s the role of technology there?” Bill: “Technology advancements have driven innovation, digitisation, cloud and more recently, AI and putting data at the centre. In every boardroom around the world, the question has become, how fast can I move? And how can I consume technology rapidly but cost-effectively? Microsoft used to talk about five clouds; now it’s one – and the services are more consumable and consistent.” Simon: “And of course, cloud reduces barriers to entry, enables innovation at pace, and of course underpins these new ecosystems. But you mentioned AI so let’s stay there for a moment; what are some of the use cases you’re seeing?” Simon Paris, Finastra (Image source: Finastra) Bill: “AI’s been in financial services for some time now – decision-making, predictive actions, fraud prevention and so on. Adding Generative AI and large language models to the mix and seeing how LLMs can be used on structured and unstructured data, and how you can interface in natural language, at scale… it’s been dramatic. And this is where the ecosystem can come in – fintechs can embed AI into their value propositions and bring different thinking to larger institutions to encourage new and different directions.” Simon: “Ecosystems, and the power of imagination… I like that a lot. So, let’s think about that with a sustainability lens – what are you seeing across the industry?” Bill: “Institutions all want to make finance more inclusive, and Generative AI is exciting in that respect, if it’s used responsibly. Microsoft’s Satya Nadella uses the example of a farmer in India that can use data and GenAI to better predict and optimise his yields, and have the financial industry serve him better, based on this data.” Simon: “It creates a virtuous circle. But there’s a power – a consumption – question. And a carbon question. How are institutions tackling that?” Bill: “We’ve all made ESG commitments without necessarily knowing the technologies we’ll need to fulfil them. So, we’re talking to institutions not just about carbon reporting, but about how to create green or investment products that offset emissions and take those to market.” Simon: “We’re seeing it too – whether our customers want software to price old-fashioned concrete vs green concrete, or price green bonds vs normal bonds. Let’s move onto the last outcome, positive societal impact. What kinds of things are you seeing?” Bill: “We see societal impact and ecosystem collaboration as connected. For example, I was talking to a customer recently about its approach to insuring V20 countries; those most vulnerable to shock. And they’re asking, how do we create a shared risk model to insure them, and distribute data to help multiple insurers make those decisions? And Finastra is doing similar things – empowering smaller institutions to distribute their capabilities to local communities or markets in a unique way. There’s constant discussion around why it takes so many institutions to move money around the world – and when you combine that with the power of data, insights and AI, well I think there’s going to be a breakthrough.” Bill Borden was interviewed as part of Finastra’s Finance is Open campaign – click here to watch the full interview. Visit Finastra TV for more interviews and insights across lending, payments, treasury & capital markets, and universal banking.

Finastra Frequently Asked Questions (FAQ)

When was Finastra founded?

Finastra was founded in 2017.

Where is Finastra's headquarters?

Finastra's headquarters is located at 4 Kingdom Street, London.

What is Finastra's latest funding round?

Finastra's latest funding round is Line of Credit.

How much did Finastra raise?

Finastra raised a total of $5.3B.

Who are the investors of Finastra?

Investors of Finastra include Carlyle, HPS Investment Partners, Ares Management, KKR, Oaktree Capital Management and 5 more.

Who are Finastra's competitors?

Competitors of Finastra include Nymbus, FintechOS, CubeLogic, Volante, Arteria AI and 7 more.

Loading...

Compare Finastra to Competitors

Nymbus operates in the financial services industry, providing alternatives to traditional banking business models. The company offers products and solutions designed to enable financial institutions of all sizes to grow and serve their customers without the need for core conversion. Nymbus primarily caters to banks and credit unions looking to launch digital banking services, create niche financial brands, or deploy innovative core banking platforms. It was founded in 2015 and is based in Jacksonville, Florida.

Mambu is a software-as-a-service (SaaS) company focused on providing a cloud banking platform within the financial services industry. The company offers a composable banking infrastructure that enables clients to create and manage lending and deposit services, as well as integrate with various application programming interfaces (APIs) for a customizable financial experience. Mambu primarily serves sectors such as banks, credit unions, and retailers looking to offer digital financial products. It was founded in 2011 and is based in Amsterdam, Netherlands.

Business Alliance Financial Services (BAFS) specializes in providing commercial lending software and services to financial institutions. Their main offerings include a cloud-based lending platform known as BLAST, along with a suite of services that support client onboarding, credit administration, and regulatory compliance. They also offer financial statement analysis, credit risk rating systems, and data analytics solutions to enhance the commercial lending process. It was founded in 2009 and is based in Monroe, Louisiana.

Abrigo focuses on providing software solutions in the financial sector. The company offers a range of products that help in lending, financial crime detection, risk management, and analytics. These products are designed to assist in various aspects such as commercial lending, consumer lending, anti-money laundering, fraud detection, and portfolio risk management. Abrigo was formerly known as Sageworks. It was founded in 2000 and is based in Austin, Texas.

BackBase is a company that focuses on providing an Engagement Banking Platform in the financial technology sector. The company offers a platform that enables banks to modernize their customer journeys and business operations, by gradually replacing or decomposing legacy systems and constructing a modern customer engagement orchestration architecture. The platform is primarily sold to the banking industry. It was founded in 2003 and is based in Amsterdam, Netherlands.

Thought Machine specializes in core banking software and operates within the financial technology sector. The company offers a cloud-native core banking platform, Vault Core, and a payment processing platform, Vault Payments, which enable banks to create and manage a wide range of financial products and payment schemes. Thought Machine's products are designed to provide banks with flexibility, control, and the ability to deploy on any cloud infrastructure. It was founded in 2014 and is based in London, England.

Loading...