We analyze Salesforce’s acquisitions, the markets they’re in, and customer satisfaction data to predict the companies Salesforce might sell and who could be tempted to buy.

Last week, it was revealed that Dan Loeb’s hedge fund Third Point had built a position in Salesforce. This follows the early January news of Paul Singer’s Elliott Management taking a multi-billion dollar stake in Salesforce. And that came quickly after the October 2022 investment by Jeff Smith’s Starboard Value. On top of all of this, ValueAct Capital CEO Mason Morfit also joined Salesforce’s board.

Taken together, that’s a lot of activist hedge funds pushing for strategic changes — including divestitures — at Salesforce.

With this pressure, private equity and strategic acquirers are evaluating Salesforce’s assets to determine which are non-core or underperforming and which may represent potential divestiture candidates.

Below we predict which Salesforce businesses might be divestiture targets based on customer perceptions of their products and look at potential buyers. In this report, we dig into:

- Salesforce’s M&A history

- Elliott Management, Starboard Value, and Third Point’s activism playbook

- Elliott Management, Starboard Value, and Third Point’s technology company activism history

- Customer perceptions of the products offered by Salesforce’s acquisitions

- The companies Salesforce is most likely to sell and the potential acquirers

Salesforce’s M&A history

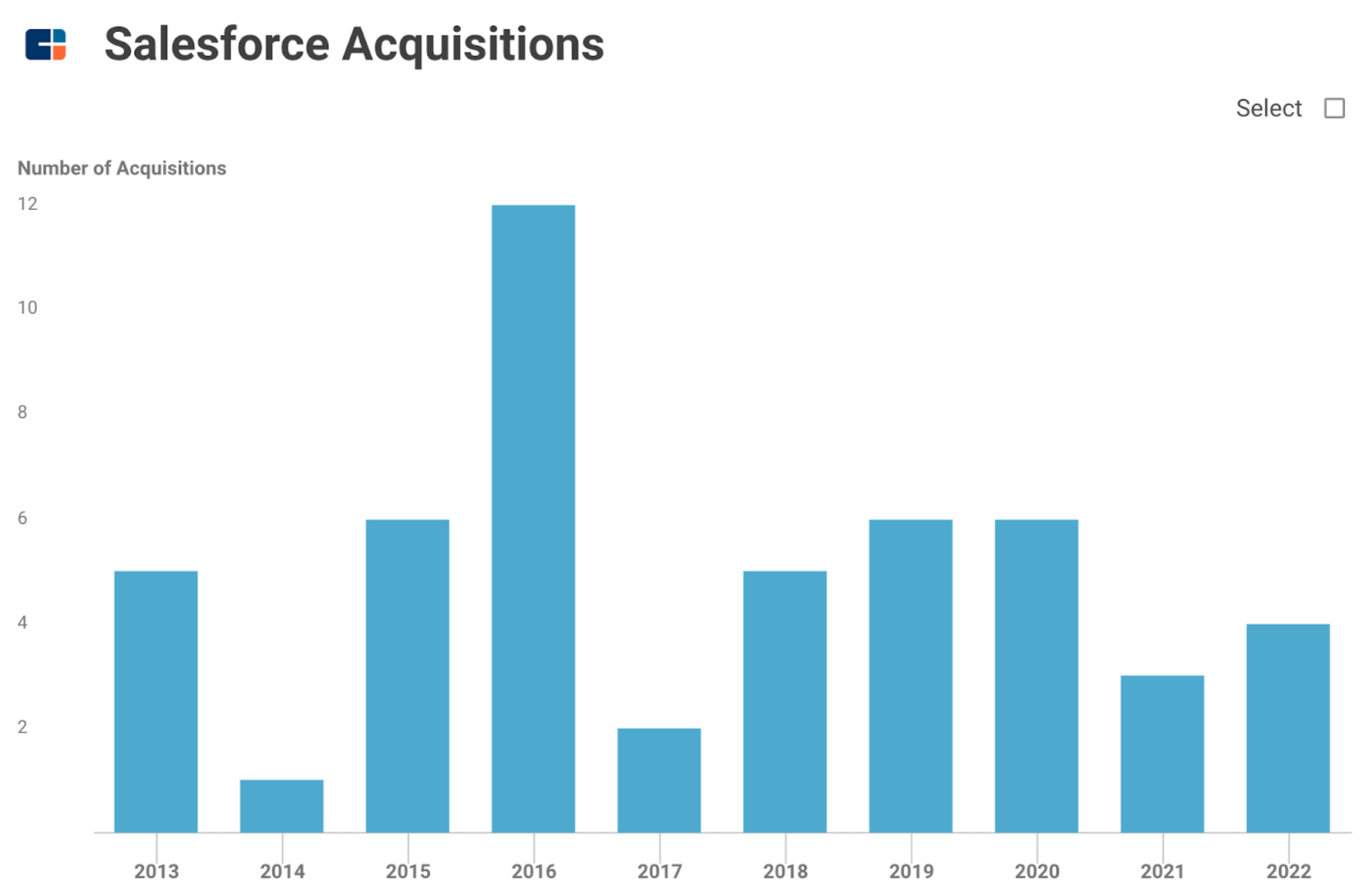

Salesforce has been an active acquirer — it completed 50 M&A deals over the last 10 years. See all of Salesforce’s acquisitions here.

The company has not been shy on the M&A front historically and has done plenty of multi-billion dollar deals — as can be seen below from Salesforce’s profile on CB Insights.

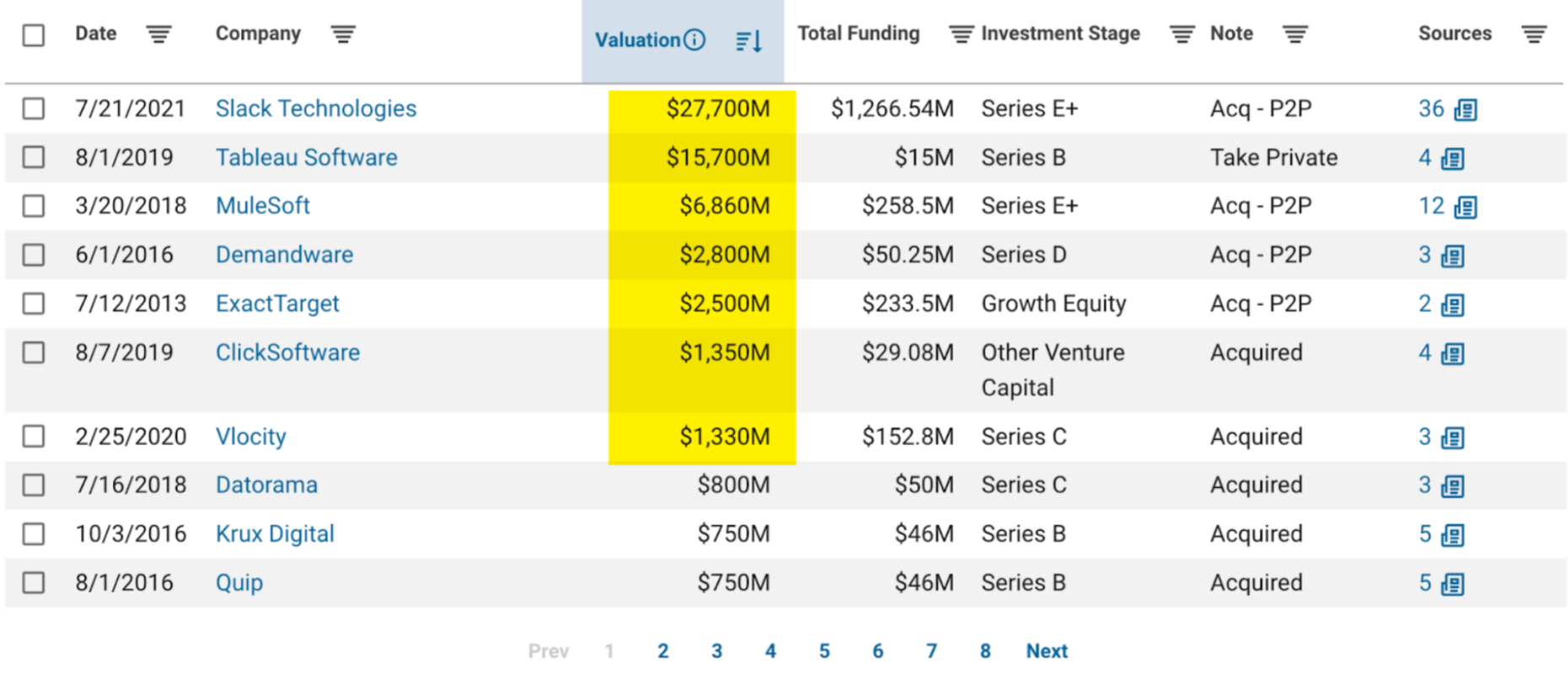

Of its deals worth over $1B, 5 out of 7 have been completed in the last 5 years including:

- Slack (acquired for $27.7B in 2021)

- Tableau (acquired for $15.7B in 2019)

- MuleSoft (acquired for $6.7B in 2018)

- ClickSoftware (acquired for $1.4B in 2019)

- Vlocity (acquired for $1.3B in 2020)

Given their size, these acquisitions present notable divestiture opportunities and are likely to draw the attention of Elliott Management, Starboard Value, and Third Point if they deploy their activism playbook.

Elliott Management, Starboard Value, and Third Point’s activism playbook

Elliott Management, Starboard Value, and Third Point are all hedge funds known for taking activist positions in public companies. Their playbook typically involves buying a significant stake in a company and then engaging with other shareholders, the management team, and the board to push for changes that they believe will improve the company’s value.

Activist investors have advocated for a broad array of changes, depending on the company, including:

- Cost cutting

- Divestitures

- Management shakeups

- Board composition changes

- Strategic shifts

- Changes to the company’s capital structure

- Taking a company private

While Elliott Management, Starboard Value, and Third Point are not technology-specific investors, each has brought their activism strategies to tech companies in the past.

Elliott Management, Starboard Value, and Third Point’s technology company activism history

Elliott Management has had several activist forays into tech, including:

- eBay where Elliott pushed for a comprehensive portfolio review, revitalizing eBay’s marketplace, operational improvements and margin expansion, more rigorous capital allocation, and changes to leadership and oversight.

- PayPal where Elliott pushed for new management and a bigger focus on profitability.

- Cognizant where Elliott pushed for a strategic review of the company’s business, leading to changes in leadership, cost cutting, and more investment in its digital business.

- Oracle where Elliott pushed for changes in the company’s management and strategy, including the appointment of new independent directors.

- AT&T where Elliott pushed for a sharper strategic focus, leaner operations, a more rigorous capital allocation framework, the sale of non-core assets, and changes to leadership and oversight.

Starboard Value’s tech activism efforts have included:

- GoDaddy in which Starboard Value built a 6.5% stake worth $800M in 2021. It pushed the company to change its balance between growth and profitability, improve capital allocation, become more disciplined around M&A, and return capital to shareholders.

- Box where Starboard Value took a 7.5% stake in 2019. Ultimately, Box won the proxy fight with Starboard Value which had sought to nominate 3 directors, remove CEO Aaron Levie, and block a $500M investment from KKR.

- Mellanox Technologies was a successful outcome for Starboard Value. In 2018, Starboard Value took a stake in the company and pushed for changes to management and strategy. Mellanox eventually sold itself to NVIDIA for $6.9B. Prior to the deal, Starboard’s activism resulted in the appointment of several directors and the setting of profit targets. In less than 18 months, Starboard sold its entire position in Mellanox for $525M — more than doubling its initial stake.

- Yahoo in which Starboard Value took a stake in 2014 and pushed for changes to the company’s management and strategy, as well as the sale of some business units. Yahoo eventually sold its core internet business to Verizon Communications for $4.8B.

Third Point’s notable tech company activism efforts have included:

- Yahoo in which Third Point amassed a stake in 2011 and where Daniel Loeb and his team were successful in appointing Marissa Mayer to the CEO role after raising issues with the company’s strategy and performance. Third Point also highlighted that prior CEO Scott Thompson had padded his resume with a non-existent CS degree in their push to remove him. In May 2012, after successfully pushing for changes in the company’s management, board of directors, and strategic direction, Third Point sold off its position for a profit.

- Sony is a company that Third Point has twice pushed for change in — in 2013 and then again in 2019. In 2019, Third Point amassed a sizable stake in Sony and urged Sony to split off its wildly profitable chip business and sell off non-core assets like Sony Financial to position itself as a major global entertainment corporation. Sony’s management did not comply with Third Point’s requests but the hedge fund’s stake still went up nearly 80% from April 2019 to August 2020.

- Intel where Third Point amassed a $1B stake in 2020. Third Point pushed Intel to improve its position as a chip supplier for PCs and data centers and to look at selling off some of its prior acquisitions. It also pushed for Intel to focus more on the retention of talented chip designers and improving morale.

With improved strategic focus being a priority among all 3 investors and given Salesforce’s aggressive M&A history, what might customer perceptions of Salesforce’s acquired products signal about potential divestiture candidates?

Customer perceptions of the products offered by Salesforce’s acquisitions

We mined software buyer interview transcripts from Yardstiq to see what customers are saying about Salesforce’s products and their competitors.

Mulesoft pricing was complicated vs. Workato

The MuleSoft pricing process, I don’t know, I think it’s Salesforce. They just took forever. I mean, my goodness, it was really difficult negotiations. Workato, on the other hand, their process was much easier from terms and conditions, pricing — very transparent, very flexible. MuleSoft, their flexibility, I wouldn’t say that’s part of their core competency. I think that just goes back to Salesforce and the way they do business.

— CIO at a $1B+ market cap consumer products company

Read the full transcript here.

Mulesoft is just too complex compared to Workato

Then it really came down to, at the end of the day, between MuleSoft and Workato. So why did we not pick MuleSoft? Pricing-wise, Workato was a little bit better, not a huge amount, but a little bit better.

But from a POC perspective, our teams really struggled with the MuleSoft platform. It’s extremely complex and our team found it really hard to really kind of grasp and come to time to market fast on these integrations. Workato, within weeks, we were able to do the integrations. A lot less complexity.

— CIO at a $1B+ market cap consumer products company

Read the full transcript here.

Mulesoft is not as strong in healthcare

I think the closest to what Redox is offering would be Jitterbit. Jitterbit is one company that comes to mind. MuleSoft is another, Dell Boomi. Maybe that’s just Boomi since I think they were spun out of Dell. So those three to me probably are the most similar to Redox. But those three companies aren’t specific to healthcare.

— COO at $10M+ funded healthcare company

Read the full transcript here.

Salesforce Einstein’s licensing model and its product accessibility are challenging for this Planhat customer

So one of the things I was recommended was Einstein in Salesforce…But then the licensing model of it was that I had to pay for every single person who wanted a copy of it, which meant that as my organization scaled, it would quickly become very, very expensive…The other thing about Einstein was it very much looked like it was more of a tool kit than it was a finished solution. So there was a lot of quite powerful functionality there, but it looked like a lot of it was going to involve me building stuff myself…And also, between you and me, I don’t think that the dashboards that you get in the general Salesforce products are very good anyway. So inevitably what I end up doing with Salesforce is I get my sales support team to dump it into Tableau and build my dashboards in Tableau.

— Chief Commercial Officer at a finance company

Read the full transcript here.

Salesforce into Slack is going well for this Gong customer

Salesforce was the main integration, as you can imagine, because in order to power the application and look at the deal flow and the timeline, you have to see the sequence of big events, both the emails and the logged calls that are not recorded, right?…Every data point that’s in the activity timeline chronologically in Salesforce is bidirectionally flowing to Gong, so that when you look at the Gong, like I said, our pipeline and forecasting tool, you can see the big picture…Gong is also integrated with our Slack, right? It’s already Salesforce, but Salesforce on Slack now. So they automatically send notifications about calls and comments to Slack channels.

— Partnerships Manager at $1B+ valuation fintech

Read the full transcript here.

This 6sense customer likes the Slack and Salesforce integrations

6sense, they were also more enterprise-ready. They had Slack integrations. And so when you’re integrating with Salesforce and Slack and you can partition by a rep and every day or every other day, when there’s an update on someone with a buyer intent or whatever signals, that rep or SDR, both would get notifications, hey, there are two companies that indicated that there’s interest. And so that was definitely better than what ZoomInfo was doing.

— Head of Sales at a cloud services provider

Read the full transcript here.

The companies Salesforce is most likely to sell and the potential acquirers

Below, we look at Salesforce’s recent large deals, predict their likelihood of divestiture, and provide rationale and potential acquirers.

Want to see more research? Join a demo of the CB Insights platform.

If you’re already a customer, log in here.