Corporate venture capital-backed deals and dollars fall to multi-year lows as CVCs shield themselves from the volatile tech market.

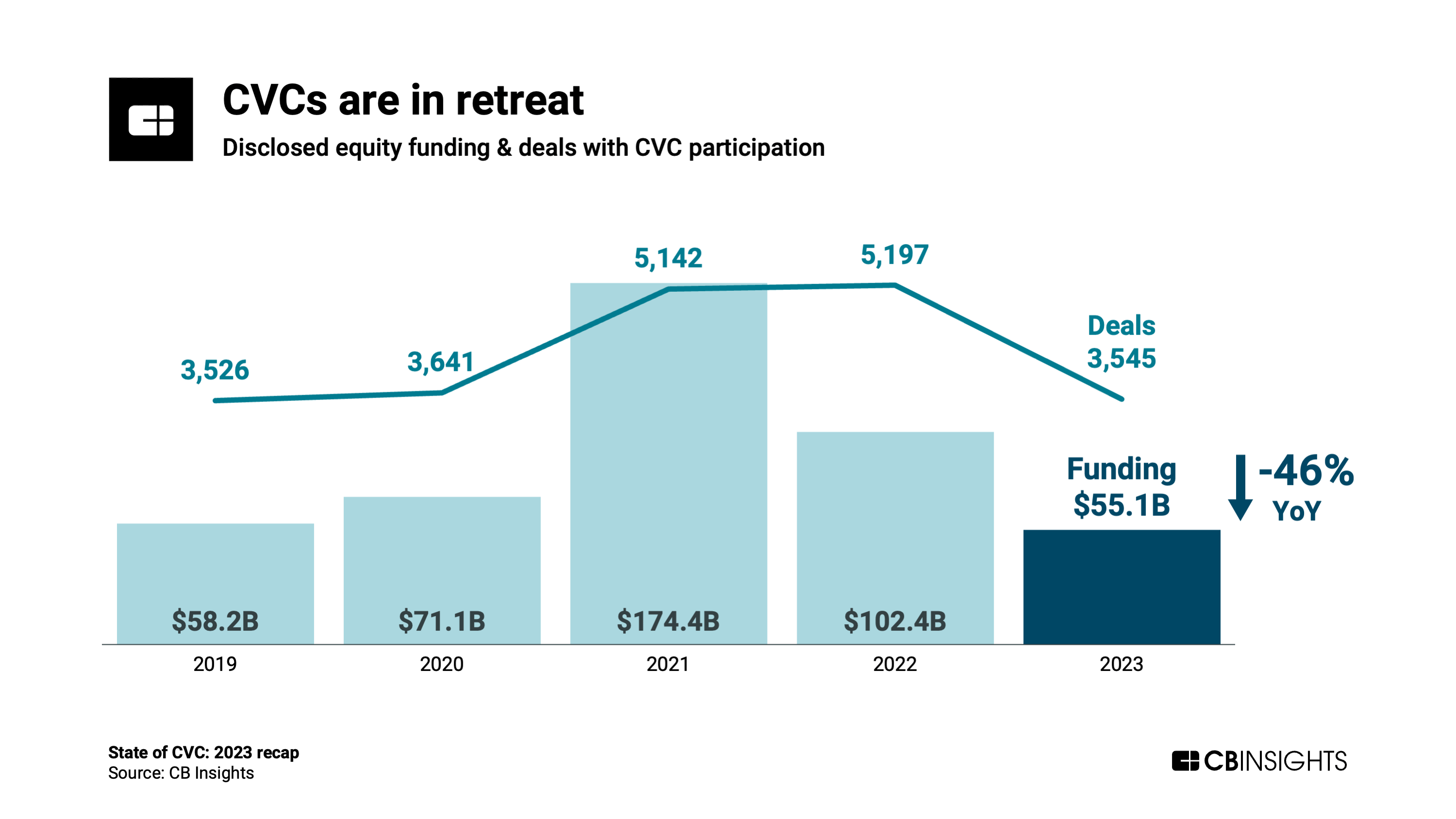

The corporate venture capital (CVC) market has constricted amid corporate belt-tightening and subdued returns from startup exits. In 2023, deals from CVCs fell to 3,545 — the lowest level since 2019 — marking a 32% drop YoY.

At the same time, fewer new CVCs are emerging: just 162 CVCs were founded in 2023 — a 6-year low.

Based on our deep dive below, here is the TLDR on the state of corporate venture:

- CVC activity is down significantly from 2021’s highs, with CVC-backed dollars and deals sinking to $55.1B across 3,545 deals in 2023. The decline in funding with CVC participation has been especially pronounced, while dealmaking, despite falling 32% YoY, remains above where it was in 2019.

- The US has been hit especially hard by the CVC retreat: Deal volume fell 25% QoQ to 233, a 6-year low, in Q4’23. This drove the US’ share of CVC deals down to just 29% among global regions — the lowest point in over a decade.

- A majority of the most active CVCs are based in Japan. The top 3 dealmakers in Q4’23 were all venture arms of Japanese financial services incumbents: Mitsubishi UFJ Capital (22 companies backed), SMBC Venture Capital (18), and Mizuho Capital (15).

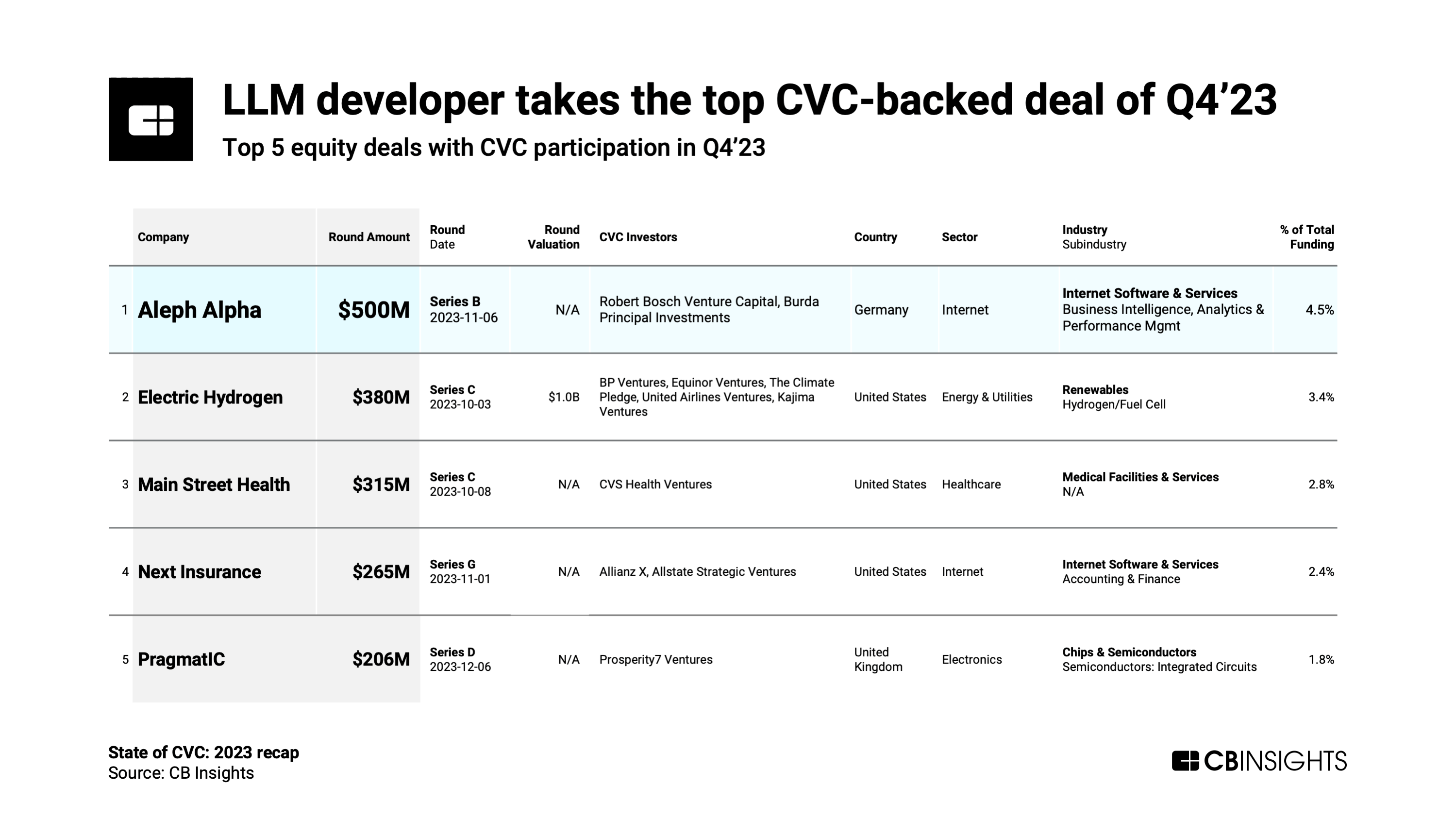

- A generative AI company took the top CVC-backed deal in Q4’23. Aleph Alpha, a Germany-based LLM developer, raised a $500M round from investors including the venture arms of Bosch and Hubert Burda Media.

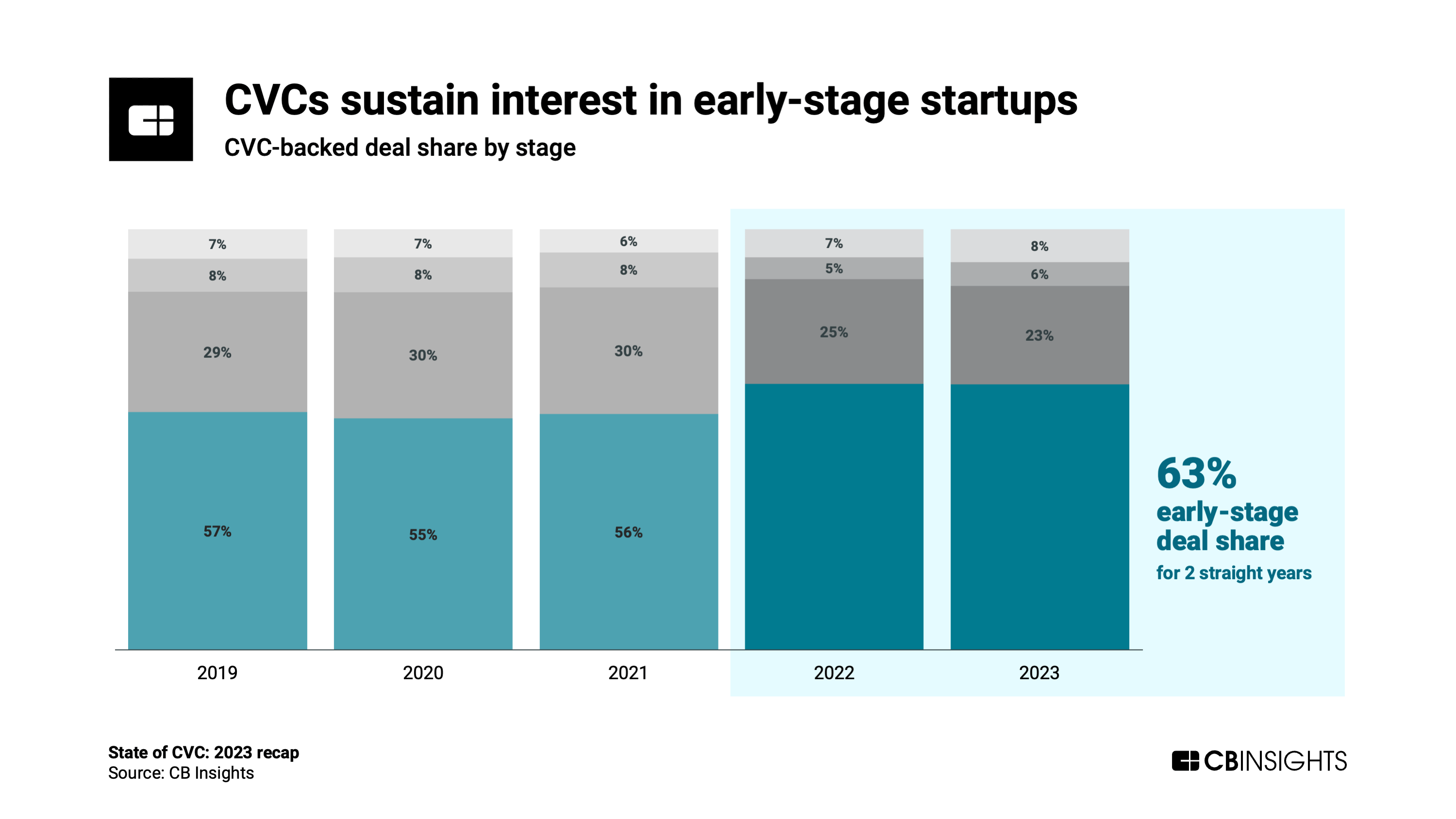

- Early-stage deal share has remained at an all-time high of 63% for 2 years running. CVCs are showing sustained interest in the earliest stages of startups, where they can form deep, long-term partnerships (and hopefully see greater financial returns in the long run).

Below, we’ll explore these themes across 5 charts.

CB Insights customers can dig into the latest corporate venture activity with this CB Insights platform advanced search.

2023 marked a precipitous drop in CVC activity globally, with funding and deals falling 46% and 32% YoY, respectively. This was roughly in line with the declines seen throughout the venture market more broadly.

Facing macroeconomic uncertainty, many CVCs are narrowing their bets on investment targets that align more closely with their parent orgs’ overarching strategies, as opposed to purely seeking financial returns.

The CVC pullback has been dramatic in the US, where deal volume slumped to just 233 in Q4’23 — a QoQ drop of 25%.

Meanwhile, Asia and Europe saw growth in CVC activity in Q4’23, signaling the potential for a rebound in 2024.

The US’ share of global CVC-backed deals slipped below 30% for the first time in over a decade — while Asia’s share ticked up to a recent high of 42%.

Globally, Japan stands out as the capital of CVC activity right now. The majority of the most active CVCs are based in the country, including the top 3 dealmakers in Q4’23: Mitsubishi UFJ Capital (22 companies backed), SMBC Venture Capital (18), and Mizuho Capital (15).

Across the broader venture market, Japan’s startups have been on a tear, notching consistently high deal counts each quarter despite the global downturn.

The generative AI boom has captured CVCs’ attention.

Germany-based Aleph Alpha, an LLM developer, took the top CVC-backed round of Q4’23 — with participation from the venture arms of Germany’s Bosch and Hubert Burda Media.

CB Insights customers can track every generative AI deal with corporate venture backing here.

One of the few bright spots in CVC right now is early-stage dealmaking. In 2023, 63% of all CVC deals were early-stage — maintaining the all-time high from 2022.

CVCs are moving earlier in the startup lifecycle as they look to establish closer ties with emerging startups.

If you aren’t already a client, sign up for a free trial to learn more about our platform.