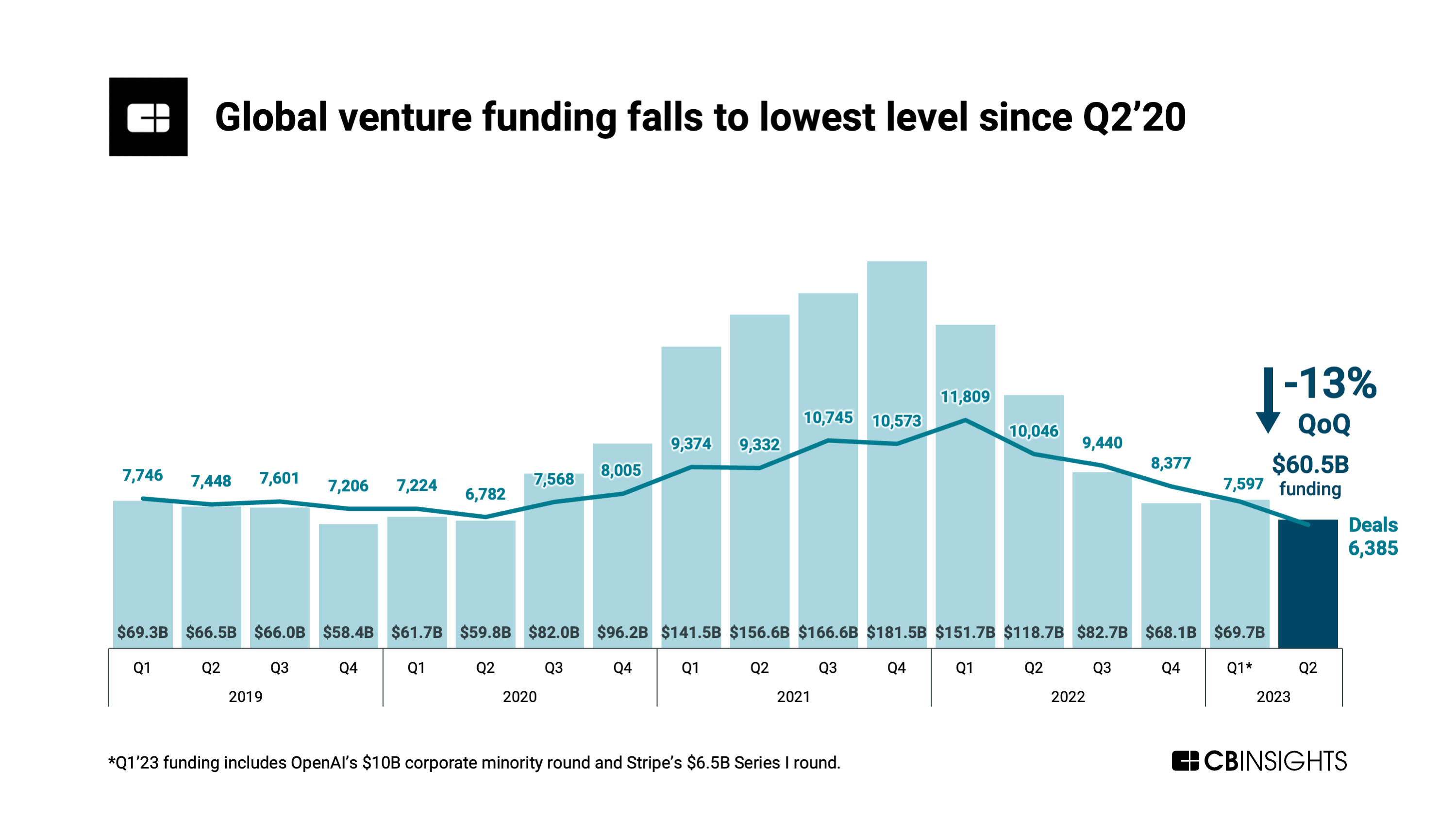

Following a slight spike last quarter, global venture funding in Q2'23 falls to its lowest level since 2020.

Global venture dollars reached $60.5B in Q2’23. That marked a 13% decline from Q1’23’s $69.7B, which was buoyed by massive, multi-billion-dollar deals to OpenAI and Stripe.

Without these Q1 deals, Q2’23 funding would have grown 14% QoQ.

Deal count, on the other hand, has continually fallen since the start of 2022. It dropped for the fifth consecutive quarter to reach 6,385 in Q2’23 — the lowest count since 2016.

Using CB Insights data, we highlight key takeaways from our State of Venture Q2’23 Report, including:

- Global venture funding drops 13% QoQ, hitting its lowest level since Q2’20.

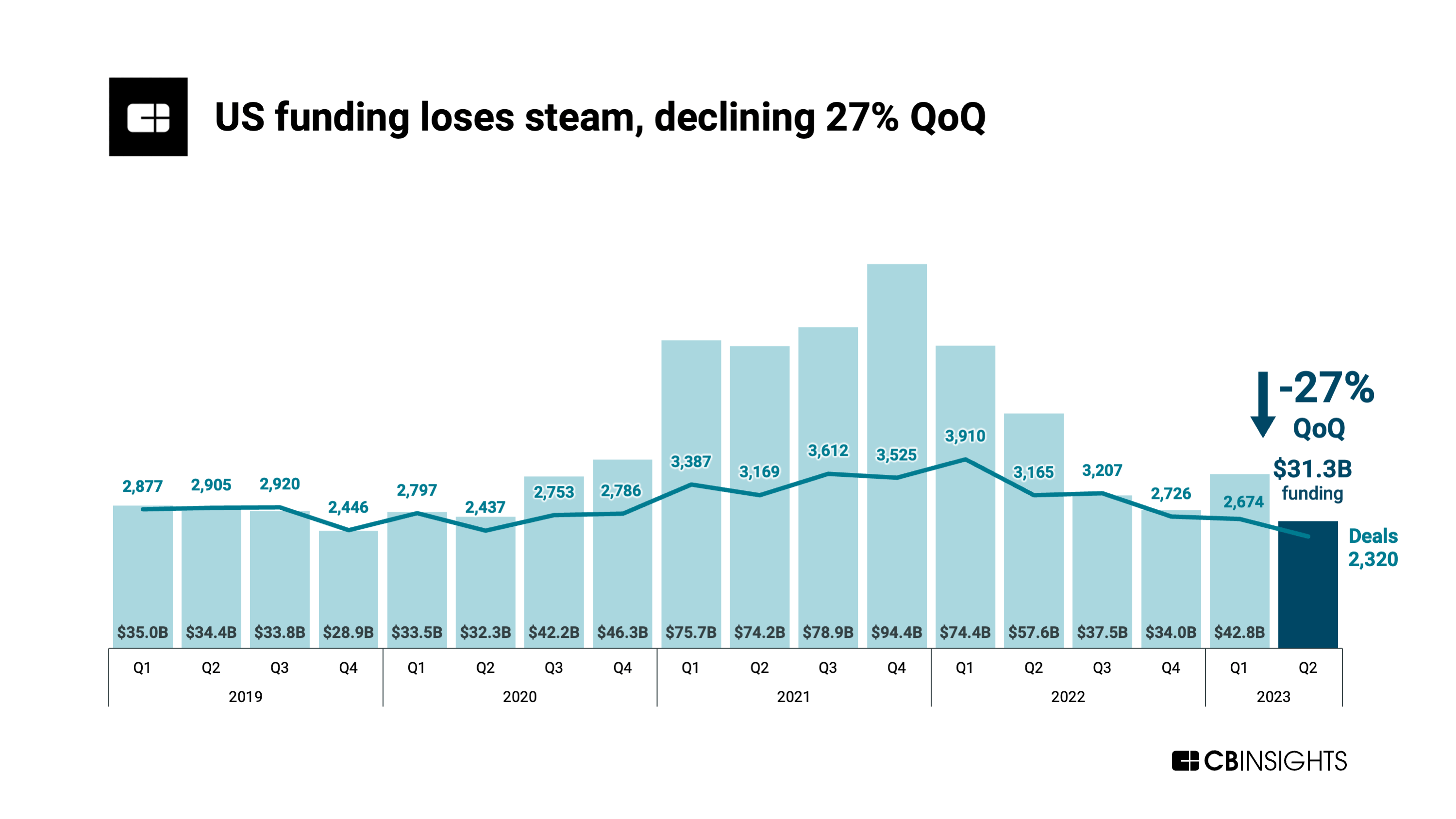

- US venture funding falls to $31.3B in Q2’23, a 27% decline QoQ.

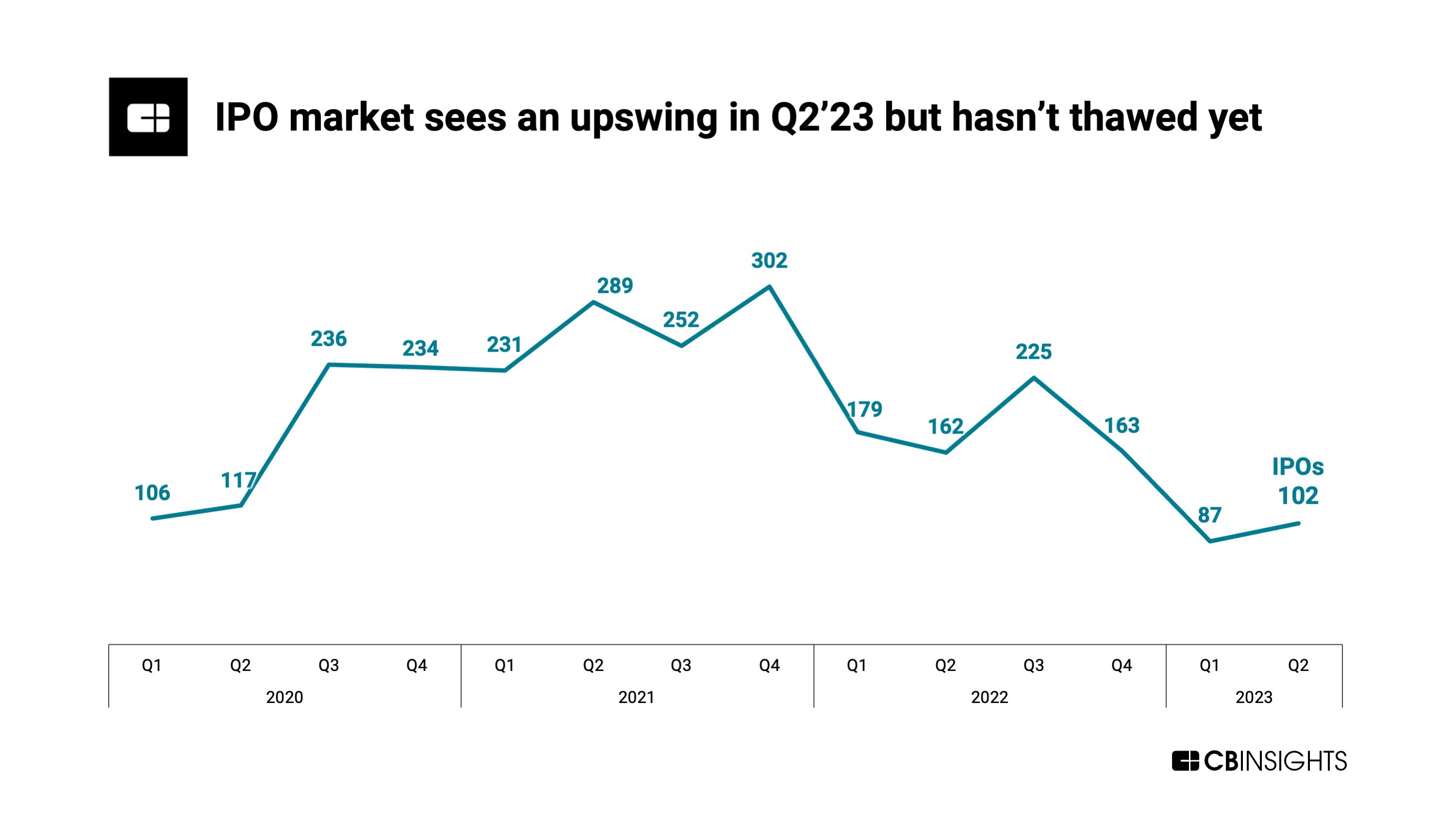

- The global IPO market reawakens, with public debuts experiencing a 17% QoQ jump in Q2’23.

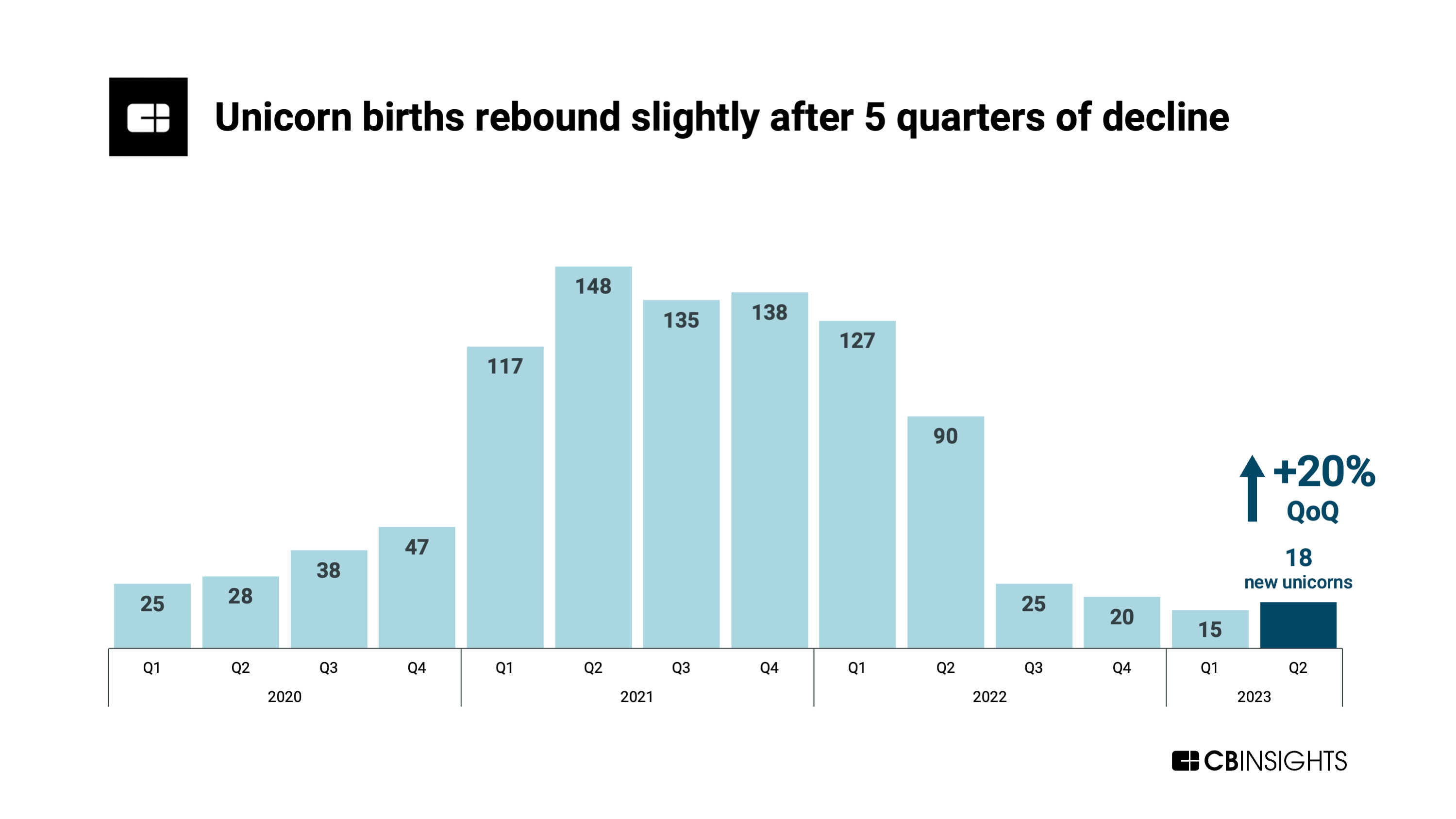

- New unicorn births jump 20% in Q2’23 after hitting a 6-year low in Q1’23.

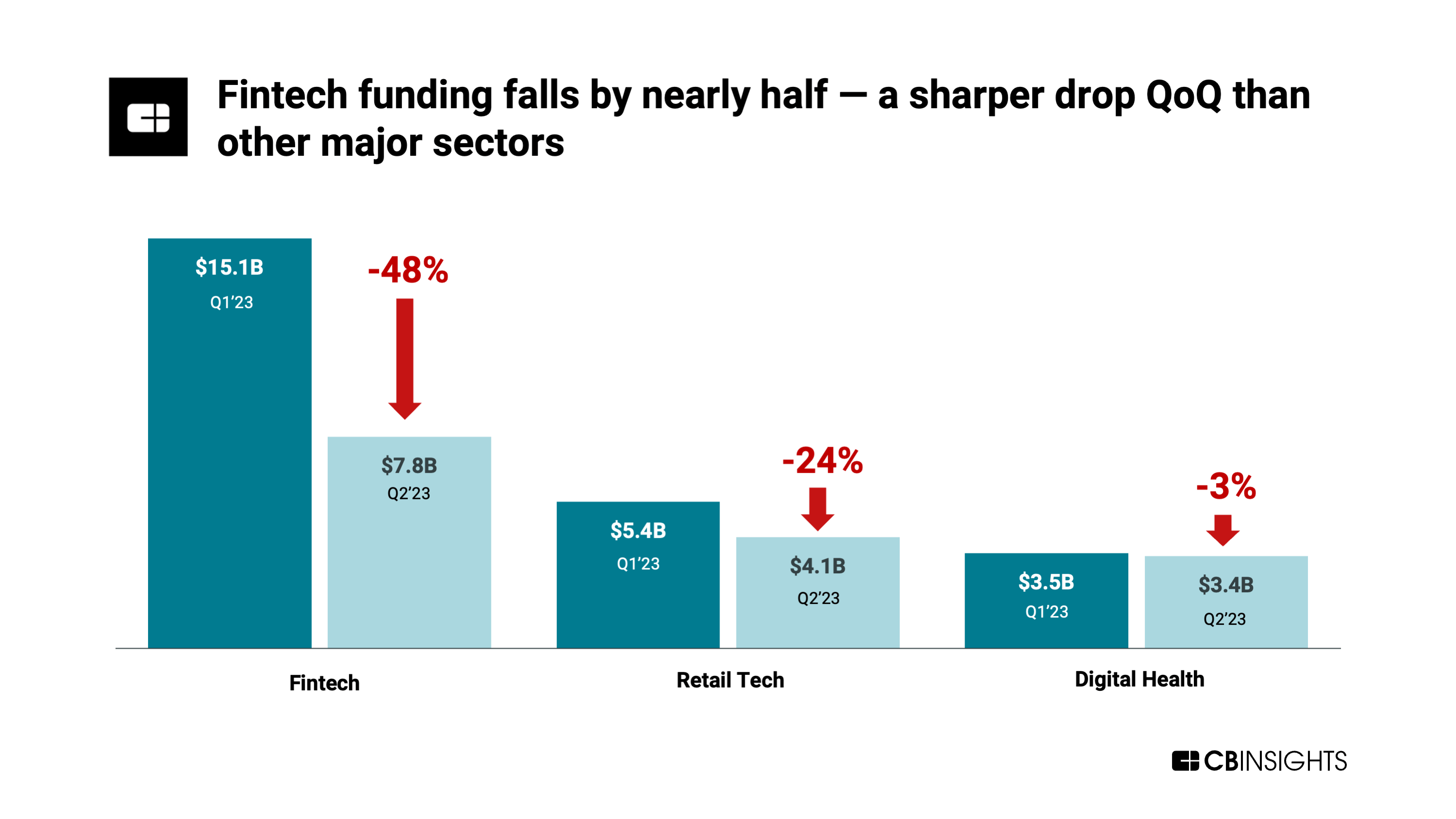

- Fintech funding falls 48% QoQ in Q2’23 — more than any other sector.

CB Insights clients can sign in and download the full report to see all the latest funding trends in venture.

Let’s dive in.

Despite inching up last quarter, global venture funding dropped 13% QoQ to hit $60.5B in Q2’23 — a 12-quarter low.

However, Q1’23’s total was boosted by huge rounds to OpenAI ($10B) and Stripe ($6.5B). Without these Q1 deals, funding would have jumped 14% QoQ in Q2’23.

Deal count also tumbled, dropping for the fifth consecutive quarter. There were 6,385 deals closed in Q2’23, a 16% decline from the previous quarter and the lowest tally since Q4’16.

At an annual level, the venture slowdown is more pronounced. H1’23 funding sits at $130.2B — less than one-third of 2022’s year-end total.

Funding activity in the US mirrored the broader venture environment in Q2’23 to an even greater extent. Q2’23 funding fell to $31.3B — a 27% decline QoQ and its lowest level in over 3 years.

Deal activity slowed as well, with US deal count falling by 13% QoQ to 2,320.

Despite the funding drop, US-based companies accounted for over half (52%) of global funding raised in Q2’23, as startups in the region continue to drive a significant amount of venture activity.

Despite the drop in deals and dollars, the IPO market showed signs of stirring in Q2’23. Global IPOs jumped 17% QoQ to hit 102 in Q2’23 after falling for 2 consecutive quarters.

The top 2 IPOs by valuation went to India-based pharma company Mankind ($6.5B) and China-based chipmaker Nexchip Semiconductor ($5.8B).

In contrast, M&A deals declined by 9% QoQ to hit 2,010 — an 11-quarter low.

Unicorn births also trended up in Q2’23. After hitting a 6-year low in Q1’23, new unicorn births rose 20% to hit 18 in Q2’23.

The US accounted for half of the quarter’s new unicorns with 9, followed by Asia with 5.

The top 2 new unicorns by valuation were China-based tea brand ChaBaiDao ($2.5B) and US-based cloud compute provider CoreWeave ($2.2B).

Despite the small jump in Q2’23, unicorn births are still rarer than ever. At 18 total, this new unicorn count marks an 80% drop from the same quarter in 2022.

Fintech saw the sharpest funding drop among sectors in Q2’23 — dollars fell 48% QoQ to hit $7.8B. This marked its lowest level since 2017.

Deal count also declined sharply, dropping by 22% QoQ in Q2’23.

The retail tech sector, meanwhile, saw funding drop 24% to $4.1B. In contrast, digital health funding remained relatively stable, falling by just 3% to $3.4B.

CB Insights clients can see all the latest investment data by signing in and downloading the full State of Venture Q2’23 Report using the sidebar.

Want to see more research? Join a demo of the CB Insights platform.

If you’re already a customer, log in here.