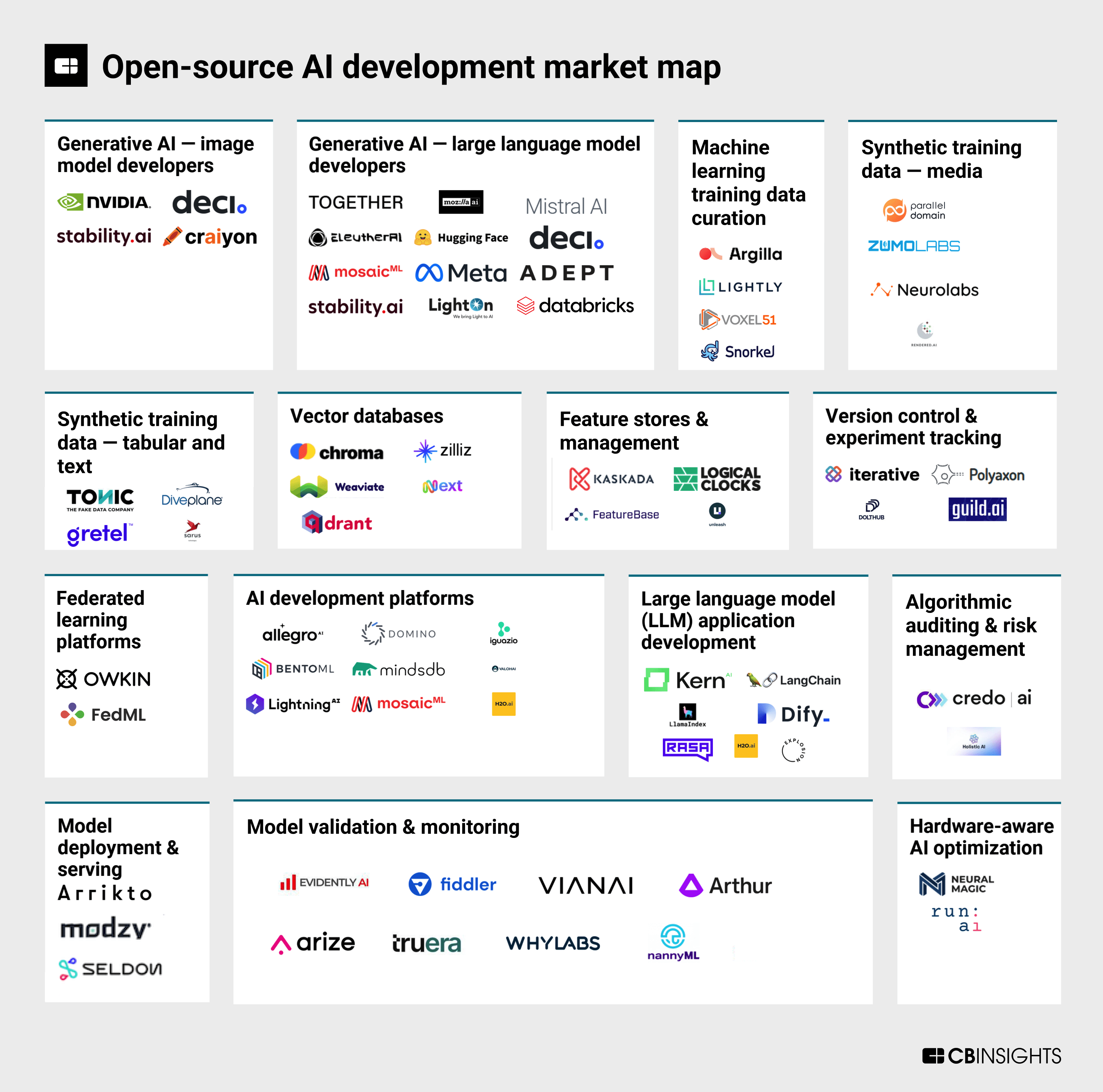

The need for AI model transparency and rapid innovation among the developer community has put open-source AI in the spotlight. We map 70+ vendors developing open-source tools to help enterprises build and deploy AI projects.

The open-source approach to AI development — which is focused on making source code available for public use and allowing a community of developers to contribute to improving software — has garnered increased attention amid the generative AI boom.

Opponents of open-source AI fear it will be misused as powerful generative technologies take center stage, to fuel cyberattacks, AI-generated hate speech, and more. However, supporters highlight the accelerated innovation that comes with a large developer community as well as the approach’s ability to boost the transparency of AI models, data, and code vulnerabilities.

This divide has played out among big tech companies vying to gain an edge in the great AI race. For instance, Meta launched its open-source large language model (LLM), Llama-2, earlier this year, while Google and OpenAI have taken closed approaches so far.

Amid the debate, mentions of open-source AI have skyrocketed in the news, and public company executives are increasingly discussing the topic on earnings calls.

Beyond open-source foundation models, a number of vendors have emerged over the years to offer open-source tools for different parts of the AI development process, from synthetic training data platforms to AI deployment software and model monitoring platforms.

In the market map below, we identify 70+ companies across 15 different categories building open-source tools to help enterprises bring AI projects from start to finish.

Note: Our map includes public, private, and recently exited companies. This market map is not exhaustive of the space.

Market comparisons

Market descriptions

Generative AI — image model developers

The generative AI — image model developers market offers foundation models and APIs for the production of visual content from scratch. These models learn from vast amounts of training data and can generate high-quality images and videos that mimic patterns and structures present in the training set. Models like generative adversarial networks (GANs) and diffusion models allow users to tailor output attributes, such as image style, content, and facial expressions, as they see fit.

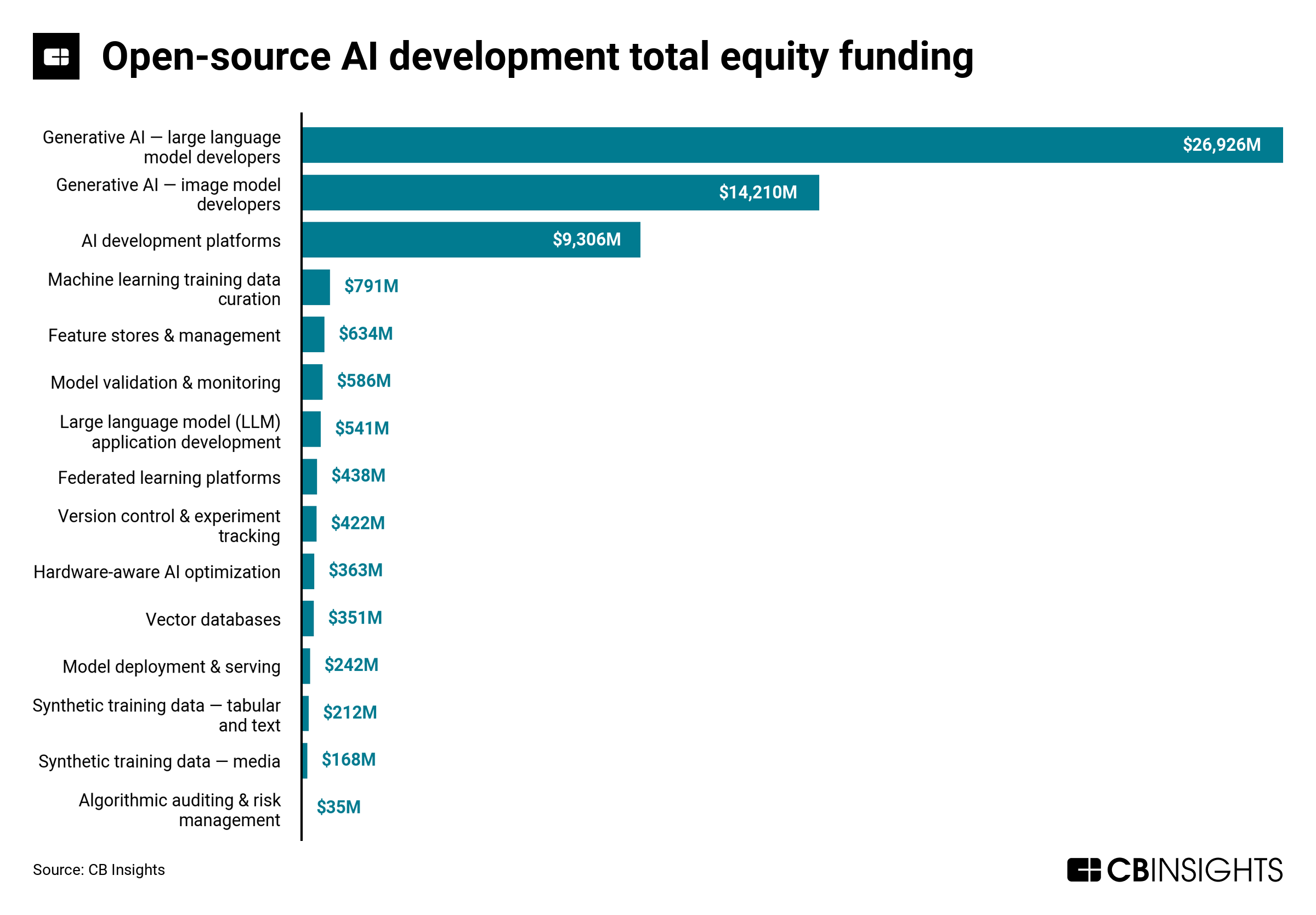

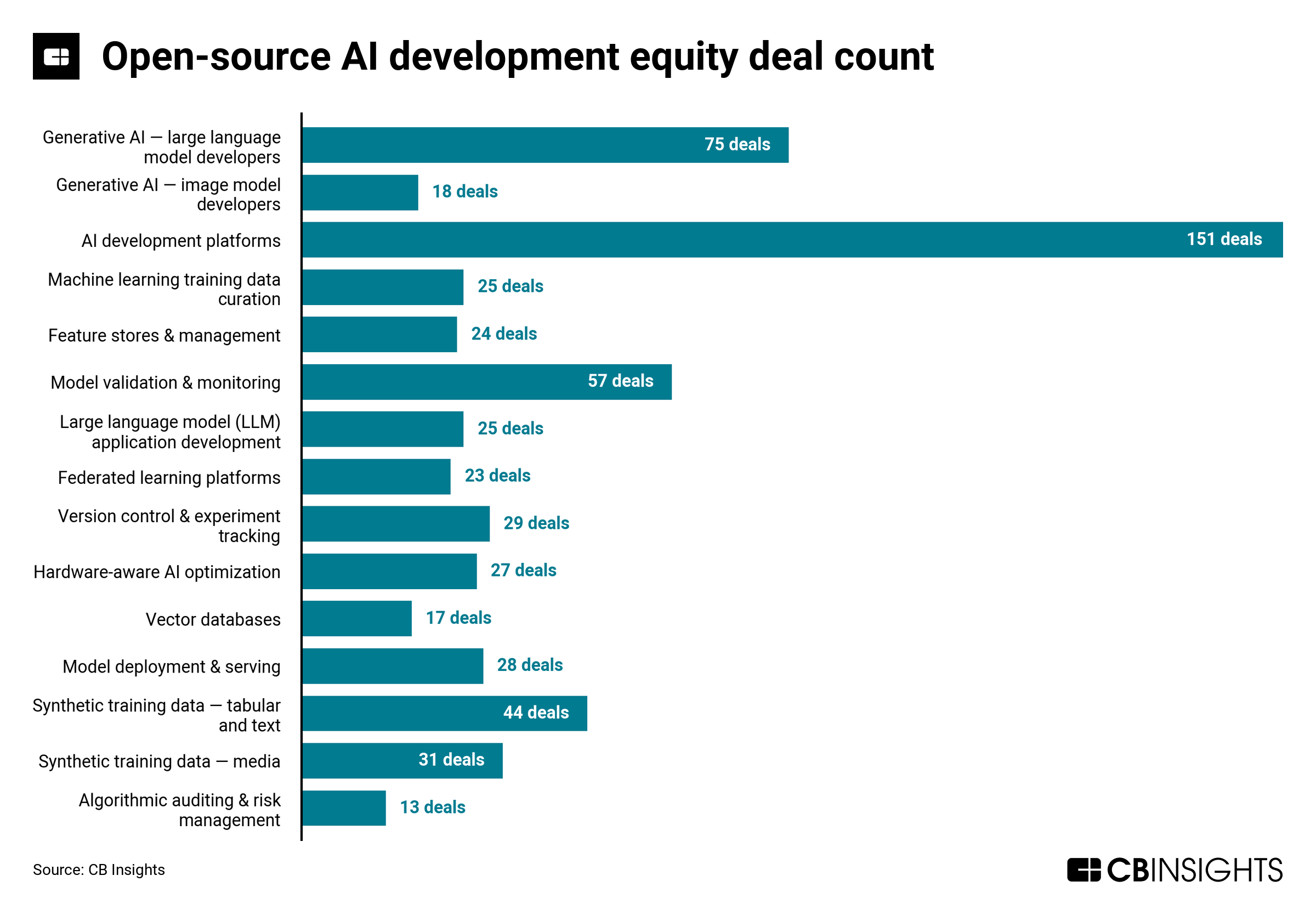

Equity funding 2023 YTD: $10B|2 deals

Headcount 1-year change: -5%

Generative AI — large language model developers

The generative AI — large language model developers market offers foundation models and APIs that enable enterprises to build natural language processing applications such as content creation, summarization, classification, chatbots, sentiment analysis, and more. Enterprises can fine-tune and customize these large-scale language models — pre-trained on vast amounts of text — for their specific use cases.

Equity funding 2023 YTD: $15.3B|20 deals

Headcount 1-year change: -5%

Featured companies:

Machine learning training data curation

The machine learning training data curation market offers solutions to support data quality control in the AI algorithm training process. These solutions help organizations complete key tasks, such as selecting the best subsets of data for training models, triaging datasets for bias, and identifying labeling errors. Ultimately, these solutions help minimize the downstream effects of poor-quality data on AI performance.

Equity funding 2023 YTD: $2M|1 deal

Headcount 1-year change: +43%

Synthetic training data — media

The synthetic training data — media market provides platforms that fabricate realistic videos and images for training AI algorithms. Synthetic data is particularly useful in cases where real video and imaging data might be sparse or hard to obtain. For example, this data can be used to help train autonomous vehicles to navigate severe weather conditions. These tools also help organizations address privacy and regulatory concerns while building AI applications.

Equity funding 2023 YTD: N/A|2 deals

Headcount 1-year change: +10%

Synthetic training data — tabular and text

The synthetic training data — tabular and text market focuses on identifying key patterns in datasets — such as patient health records or customer purchase histories — to generate new, anonymous datasets that retain the key properties of the originals. The anonymity of synthetic data enables secure and compliant collaboration. The market is driven by the increasing demand for high-quality data that is compliant with regulations such as the GDPR and the CCPA. The use of synthetic data also eliminates the need for time-consuming anonymization, labeling, and masking techniques.

Equity funding 2023 YTD: $11M|3 deals

Headcount 1-year change: +7%

The vector databases market focuses on providing databases optimized for high-dimensional, vector-based data. These databases are designed to efficiently store, manage, and query large volumes of vectors — i.e., mathematical representations of data points in multidimensional space. Vector databases cater to a wide range of applications, including machine learning, natural language processing, recommendation systems, and similarity search.

Equity funding 2023 YTD: $176M|5 deals

Headcount 1-year change: +68%

The feature stores & management market provides enterprises with a central repository for features and related metadata, enabling AI teams to share features and ensure definition consistency. These tools enable easy access, reuse, and tracking for compliance purposes. Feature stores also transform incoming raw data into usable features that are made available to AI algorithms in real time.

Equity funding 2023 YTD: No deals

Headcount 1-year change: +6%

Version control & experiment tracking

The version control & experiment tracking market provides tools that allow AI teams to collaborate by automatically tracking, logging, and comparing thousands of iterations of ML experiments. Teams can keep records of changes made to training data, source code, and model parameters as well as track all ML-related metadata. Some vendors focus primarily on data version control (i.e., tracking changes made to data used in AI experiments), while others provide end-to-end experiment management. Experiment management tools make AI research reproducible — which is necessary for the creation of auditable and explainable models.

Equity funding 2023 YTD: $50M|1 deal

Headcount 1-year change: +6%

The federated learning platforms market enables model training across multiple decentralized devices or data sources. Companies can harness federated learning to develop AI models collaboratively without centralizing sensitive data. This approach helps organizations maintain robust security and compliance standards in order to mitigate the risk of data breaches and privacy violations. These platforms are being used in various sectors, such as healthcare and finance.

Equity funding 2023 YTD: $31M|3 deals

Headcount 1-year change: +51%

The AI development platforms market offers solutions that serve as one-stop shops for enterprises that want to develop and launch in-house AI projects. Vendors in this space enable organizations to manage all aspects of the AI lifecycle — from data preparation, training, and validation to model deployment and continuous monitoring — through a single platform in order to facilitate end-to-end model development. Some vendors offer “drag-and-drop” interfaces or “plug-and-play” solutions that enable teams without in-depth AI expertise to build AI projects.

Equity funding 2023 YTD: $837M|11 deals

Headcount 1-year change: +21%

Large language model (LLM) application development

The large language model (LLM) application development market includes tools for customizing and refining pre-trained language models for specific tasks and industries. Fine-tuning involves adjusting the weights of a model or training the model on task-specific data to make it more accurate and adaptable for particular applications. Companies in this market offer services and tools to fine-tune large language models like GPT-3 or open-source models.

Equity funding 2023 YTD: $314M|11 deals

Headcount 1-year change: +36%

Algorithmic auditing & risk management

The algorithmic auditing & risk management market provides solutions for evaluating and mitigating risks associated with algorithmic decision-making. These tools enable organizations to ensure algorithmic fairness, transparency, and regulatory compliance. Vendors in this space take a multifaceted approach to derisking AI, which includes data auditing, model validation, metadata tracking, and post-production monitoring.

Equity funding 2023 YTD: $1M|2 deals

Headcount 1-year change: +22%

The model deployment & serving market bridges the gap between data science and DevOps teams by taking trained machine learning models and putting them into production. Vendors offer tools for machine learning deployment on Kubernetes as well as serverless technology that can be used to deploy AI in cloud and on-prem environments. Most deployment vendors provide continuous model monitoring and governance tools.

Equity funding 2023 YTD: $29M|2 deals

Headcount 1-year change: -7%

The model validation & monitoring market provides solutions that continuously monitor the performance of AI models and provide real-time visibility into model behavior. These solutions track outliers in predictions, potentially biased outcomes, and suspected adversarial attacks. Demand for these solutions is driven by the fact that AI model performance can degrade over time if it continuously encounters real-world data that varies significantly from its training data.

Equity funding 2023 YTD: $20M|3 deals

Headcount 1-year change: +13%

Hardware-aware AI optimization

The hardware-aware AI optimization market provides software solutions that optimize AI algorithms and models to run efficiently on available hardware, such as GPUs and CPUs. These solutions also allow enterprises to compress neural networks to run on edge devices or on-prem servers. With optimization tools, businesses can speed up AI deployments, reduce prediction latency, and improve model performance.

Equity funding 2023 YTD: No deals

Headcount 1-year change: +22%