Rapyd

Founded Year

2016Stage

Series E | AliveTotal Raised

$775MValuation

$0000Last Raised

$300M | 3 yrs agoRevenue

$0000Mosaic Score The Mosaic Score is an algorithm that measures the overall financial health and market potential of private companies.

-58 points in the past 30 days

About Rapyd

Rapyd is a fintech company specializing in global payment processing and financial technology solutions. The company offers a platform for businesses to accept payments online, send payouts, and manage multi-currency accounts, with a focus on simplifying financial transactions across borders. Rapyd's services cater to various sectors including eCommerce, marketplaces, and the gig economy. Rapyd was formerly known as CashDash. It was founded in 2016 and is based in London, England.

Loading...

Rapyd's Product Videos

ESPs containing Rapyd

The ESP matrix leverages data and analyst insight to identify and rank leading companies in a given technology landscape.

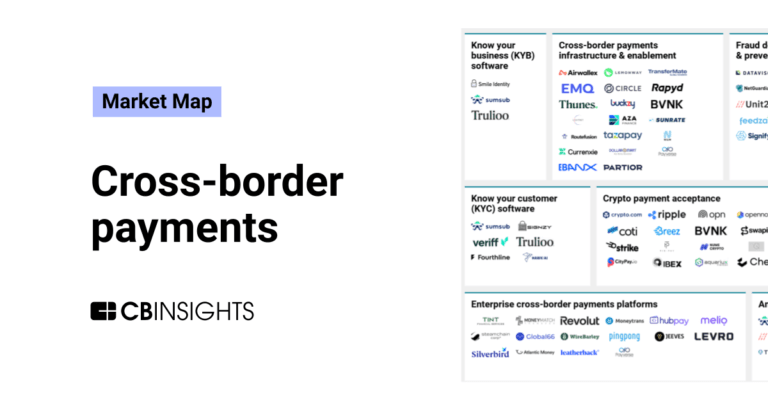

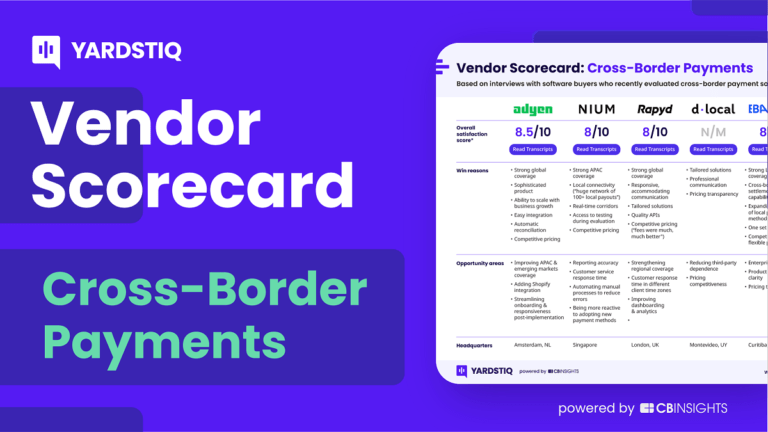

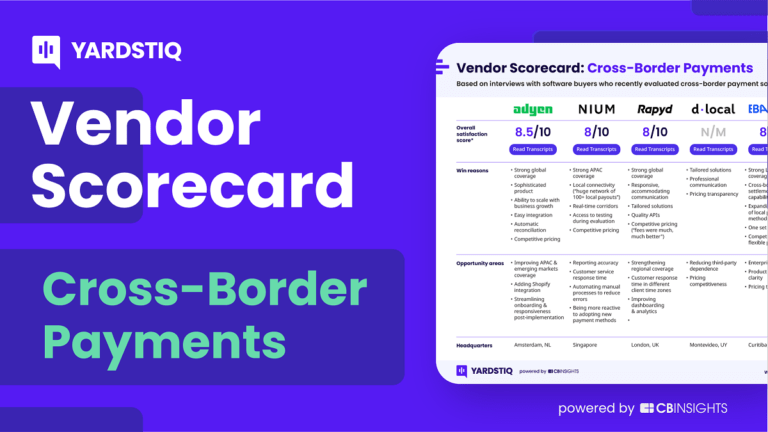

The cross-border payments infrastructure & enablement market allows businesses to send and accept global payments on their own websites and payment platforms. The companies in this market offer APIs that allow businesses to process payments across currencies and platforms (such as mobile), make payouts, verify user identities, issue credit cards, and more. Some companies also enable businesses to …

Rapyd named as Challenger among 15 other companies, including FIS, Nium, and Checkout.com.

Rapyd's Products & Differentiators

Rapyd Collect

A single integration that connects your business to hundreds of payment methods worldwide.

Loading...

Research containing Rapyd

Get data-driven expert analysis from the CB Insights Intelligence Unit.

CB Insights Intelligence Analysts have mentioned Rapyd in 14 CB Insights research briefs, most recently on May 8, 2024.

May 8, 2024

The embedded banking & payments market map

Dec 14, 2023

Cross-border payments market map

Jan 23, 2023 report

Top cross-border payments companies — and why customers chose themExpert Collections containing Rapyd

Expert Collections are analyst-curated lists that highlight the companies you need to know in the most important technology spaces.

Rapyd is included in 9 Expert Collections, including E-Commerce.

E-Commerce

11,263 items

Companies that sell goods online (B2C), or enable the selling of goods online via tech solutions (B2B).

Unicorns- Billion Dollar Startups

1,249 items

SMB Fintech

1,648 items

Payments

3,034 items

Companies in this collection provide technology that enables consumers and businesses to pay, collect, automate, and settle transfers of currency, both online and at the physical point-of-sale.

Fintech

13,413 items

Excludes US-based companies

Fintech 100

749 items

250 of the most promising private companies applying a mix of software and technology to transform the financial services industry.

Latest Rapyd News

Oct 30, 2024

February 13, 2019 The modern global economy demands increasing levels of flexibility and adaptability — often beyond the current capabilities of financial services providers. A single purchase might involve a customer in France using an e-wallet to buy a product from a merchant in Brazil who accepts payments in real and, in turn, disburses funds to a supplier in Indonesia in rupiah. Rapyd has built a platform that makes it easier to execute transactions like this one, and in general, reduces friction associated with global payments. Rapyd was founded in late 2015 by Arik Shtilman, a serial entrepreneur who bootstrapped his previous company, ITNAVIGATOR, and sold it to Avaya in 2013. Rapyd aggregates local payment providers into a global “network of networks” that allows merchants, on-demand gig platforms, and online financial services providers to digitally enable and scale common local payment methods around the world. Through a single API, Rapyd offers a unified set of fintech and payments capabilities, enabling its customers to accept alternative payment methods (e.g. cash, bank transfers, e-wallets, local debit, etc.) and perform both local cash collection and disbursement. Beyond this, Rapyd provides tokenized identity management and compliance solutions (KYC/AML), as well as software for e-wallet and FX management. Today, we are excited to announce that, along with GC portfolio company and close partner Stripe, we’ve co-led a $40M Series B financing in Rapyd. Our core thesis is that Rapyd is bridging the gap between robust economies and an increasingly important group of stakeholders in global commerce: the unbanked and the non-credit/debit card economy. This group represents over 2 billion people and ~72% of online payments today (local bank transfers, e-wallets, and cash). As global e-commerce merchants, sharing and gig economy marketplaces, banks, and telcos expand their global footprint, they face considerable challenges: making and receiving payments in hundreds of countries and currencies; navigating regulatory environments; supporting the locally preferred payment methods. The widespread prevalence of cash-based economies and payments, especially in emerging markets, plus the rise of alternative payment methods like e-wallets, instant payments, mPesa, UPI, iDEAL, etc., have created a huge challenge for global businesses as they scale. It is also expensive, impractical, and prohibitive from a regulatory perspective to connect directly to each and every end-point in local markets. Enter Rapyd, a company that has spent the last few years building out a “network of networks” via integrations with local payment network partners around the world, including a heavy focus on emerging markets. To date, Rapyd has amassed a global network of 1.6 million cash collection endpoints (i.e. ATMs and convenience stores) and ~100 different e-wallets to power non-card-based payments in 65+ currencies in ~150+ countries. By allowing customers to simply plug into its end-to-end global alternative payment menthods (APM) network instead of building it themselves, Rapyd provides access to billions of end-customers, as well as to a universe of contractors and suppliers that participate on global marketplaces. Rapyd powers a wide variety of use cases, including: enabling remittance companies and online lenders to payout money, allowing telcos to offer e-wallets and payment solutions or improve existing deployments, helping global marketplaces receive cash and APM payments as well as make payments to sellers or contractors, and enabling large banks to expand their product offering to their global business clients. While credit and debit cards dominate both e-commerce purchases and point-of-sale (POS) more broadly in the United States (63% and 75%, respectively), this is not the case in the rest of the world. Much of our world runs on cash. Globally, there were $19 trillion of cash payments and $20 trillion of cash deposits made in 2016, while 31% of all global workers are paid only in cash. 31% of POS transactions and 52% of bills are paid via cash. In some regions (especially Asia), we have seen a massive rise in digital payments (bank transfer and e-wallet), where penetration has leapfrogged the Western world. There are 100+ e-wallet companies around the world, and 17% of e-commerce outside the U.S. is done via e-wallet payments. More than half of e-commerce transaction volume is made via e-wallet and other alternative payment methods. Cash and alternative payment trends look quite different across regions. Asia is expected to see a huge shift from cash to e-wallets in the coming years, as e-wallets expand to 66% of regional e-commerce and 42% of POS transactions by 2022. Cash will remain prevalent in Latin America, continuing to represent 36% of POS transactions (down from 58% today). E-wallets and bank transfers will drive EMEA e-commerce, representing 24% and 20% of transactions by 2022, while cash at POS (which dominates markets like the UEA and Nigeria, at 70% and 97% of payments, respectively), will shift from 47% of total POS payments to a still-meaningful 30%. Clearly, the opportunity to tap into international consumers who are using cash and APMs both online and at point-of-sale is large and growing fast. Rapyd is at the forefront of this trend and will no doubt help global players in commerce, transportation, banking, and telecom expand their footprint, access more customers, and improve their customer offerings. — Adam Valkin, Addie Lerner, Matt Brennan & GC Team

Rapyd Frequently Asked Questions (FAQ)

When was Rapyd founded?

Rapyd was founded in 2016.

Where is Rapyd's headquarters?

Rapyd's headquarters is located at 119 Marylebone Road, London.

What is Rapyd's latest funding round?

Rapyd's latest funding round is Series E.

How much did Rapyd raise?

Rapyd raised a total of $775M.

Who are the investors of Rapyd?

Investors of Rapyd include Target Global, General Catalyst, Durable Capital Partners, Tal Capital, Spark Capital and 20 more.

Who are Rapyd's competitors?

Competitors of Rapyd include Conduit, Colleen AI, Nium, Alviere, Tazapay and 7 more.

What products does Rapyd offer?

Rapyd's products include Rapyd Collect and 3 more.

Who are Rapyd's customers?

Customers of Rapyd include Uber, Google, Hotmart, Rappi and GoTrade (TR8 Securities).

Loading...

Compare Rapyd to Competitors

Stripe operates as a technology company that specializes in online payment processing and financial infrastructure for Internet businesses. The company provides a suite of products that enable businesses to accept payments, manage billing and subscriptions, handle in-person transactions, and integrate various financial services into their operations. Its platform is designed to support startups, enterprises, and everything in between with scalable, API-driven solutions. Stripe was formerly known as DevPayments. It was founded in 2010 and is based in South San Francisco, California.

Nium specializes in modern money movement within the financial technology sector. Its main offerings include a platform for cross-border payments, card issuance services, and banking-as-a-service solutions, designed to facilitate global financial transactions for businesses. Nium primarily serves financial institutions, travel companies, payroll providers, spend management platforms, and global marketplaces. Nium was formerly known as InstaReM. It was founded in 2014 and is based in Singapore.

BlueSnap, formerly Plimus, is a flexible payment solutions provider delivering a customizable platform to global online businesses such as software publishers, web hosting companies, and online retailers. BlueSnap builds and manages online businesses for software publishers, web hosting companies and online retailers. A business can choose BlueSnap hosted application that spans the entire e-Commerce lifecycle, or it can deploy the BlueSnap API which allows retailers to integrate the technology with existing solutions. Using BlueSnap software, retailers can deliver newsletters to customers, coupons and promotions, realtime reporting, and live chat amongst other features.

Checkout.com offers companies to accept payments around the world through one application program interface. It facilitates an integrated payment processing platform allowing the processing of payments in real-time, sending payouts, issuing, processing, and managing card payments. It also offers fraud prevention and secure authentication. The company was formerly known as Opus Payments. It was founded in 2012 and is based in London, United Kingdom.

Payall operates as a cross-border payment processor for banks operating in the financial technology sector. The company offers automated compliance and risk management solutions to facilitate international transactions. Payall's technology provides a global platform with accounts and special-purpose payment processing for global payments, along with payout options for recipients. It was founded in 2018 and is based in Miami Beach, Florida.

EBANX is a company focused on providing cross-border payment solutions and services for global companies looking to succeed in emerging markets. The company offers a comprehensive payment platform that supports over 100 payment methods, enabling businesses to reach customers in 29 countries across Latin America, Africa, and India. EBANX's platform is designed to simplify operations for its clients, offering features such as instant market access, advanced fraud and risk management, and a commitment to innovation with a suite of payment services tailored for various digital-driven industries. It was founded in 2012 and is based in Curitiba, Brazil.

Loading...