Yapily

Founded Year

2017Stage

Incubator/Accelerator - II | AliveTotal Raised

$69.4MMosaic Score The Mosaic Score is an algorithm that measures the overall financial health and market potential of private companies.

-53 points in the past 30 days

About Yapily

Yapily is an open banking infrastructure platform that specializes in providing secure connectivity between customers and banks across Europe. The company offers services that enable access to financial data and the initiation of payments, aiming to facilitate the creation of personalized financial experiences. Yapily primarily serves industries such as payment services, i-gaming, accounting, lending and credit, crypto, property technology (PropTech), investing, and digital banking. Yapily was formerly known as Acacia Connect. It was founded in 2017 and is based in London, United Kingdom.

Loading...

Yapily's Product Videos

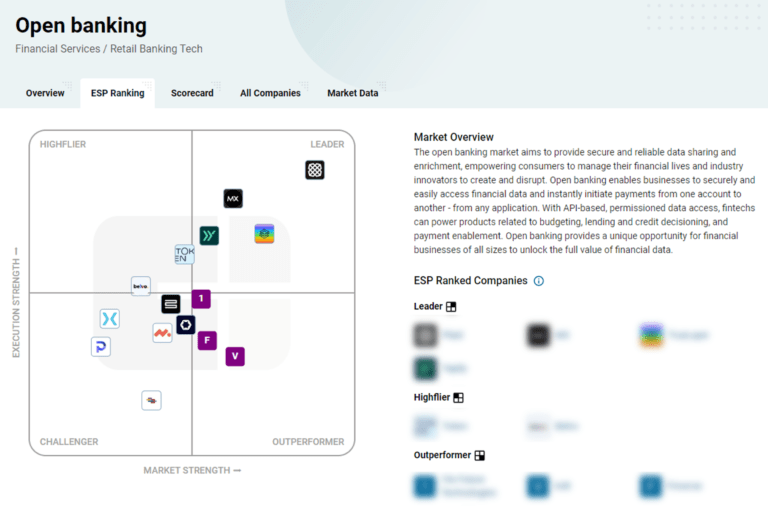

ESPs containing Yapily

The ESP matrix leverages data and analyst insight to identify and rank leading companies in a given technology landscape.

The open banking solutions market aims to provide secure and reliable data sharing and enrichment, helping consumers to manage their financial lives and industry innovators to create new products. Open banking solutions enable businesses to securely and easily access financial data and instantly initiate payments from one account to another — from any application. With API-based, permissioned data…

Yapily named as Leader among 15 other companies, including Tink, Fiserv, and Volt.

Yapily's Products & Differentiators

Payments

Yapily Payments: Single account-to-account payments from over 2000 banks across 19 markets. Used directly by merchants and platforms or PSPs offering open banking as a cheaper payment method to create better user experiences and boost conversions. Yapily Bulk (available in beta UK only): Single bulk payment to multiple recipients at once. Used by PSPs or platforms to pay suppliers, contractors, and run payroll with open banking. Yapily VRP sweeping and non-sweeping (available in beta UK only): Variable recurring payments (VRP) allows users to collect variable payments on an ongoing basis without needing to authorise each payment every single time. It offers a smarter, flexible version of direct debits and will enable businesses to offer faster checkout and manage subscription services.

Loading...

Research containing Yapily

Get data-driven expert analysis from the CB Insights Intelligence Unit.

CB Insights Intelligence Analysts have mentioned Yapily in 3 CB Insights research briefs, most recently on Jan 4, 2024.

Jan 4, 2024

The core banking automation market map

Expert Collections containing Yapily

Expert Collections are analyst-curated lists that highlight the companies you need to know in the most important technology spaces.

Yapily is included in 3 Expert Collections, including Fintech.

Fintech

13,413 items

Excludes US-based companies

Fintech 100

250 items

250 of the most promising private companies applying a mix of software and technology to transform the financial services industry.

Digital Banking

979 items

The open banking ecosystem is facilitated by three main categories of startups including those focused on banking-as-a-service, core banking, and open banking startups (i.e. data aggregators, 3rd party providers). These are primarily B2B companies, though some are also B2C.

Latest Yapily News

Oct 28, 2024

28 Oct 2024 Open Banking data has been a “powerful tool” for the UK’s SMEs, but the shift to Open Finance and Smart Data will provide a “more full picture” to ensure businesses get “better outcomes for themselves”, according to Yapily’s Nicole Green. Green, who is vice president API products, strategy, operations and policy at the Open Banking infrastructure provider was speaking at a panel discussion on Day Two of Open Banking Expo UK & Europe. Speaking on the Main Stage on 16 October, Yapily’s Green was joined by Emma Zaraisky, payments partnership development manager at Google and Sophie Hossack, Allica Bank’s head of partnerships for the session titled ‘Fueling SME growth and innovation through Open Banking’, during which they also discussed the potential to improve the payments experience for SMEs and their customers. “Getting that visibility of cashflow, understanding and aggregating accounts has been something that’s been very powerful as a tool,” said Green, when asked how Open Banking is already supporting SMEs to scale and grow. “There’s a lot of opportunity that’s coming. CFIT had the SME Lending Taskforce. I think there’s starting to be this look at how can we bring in both the current account, but also the credit card data, as a data point to use in a lending decision.” She added: “And then that expansion into other data sources that will be coming with Open Finance, hopefully, and Smart Data in general to usher in a more full picture. So that businesses can really understand fully where they stand, and then take that information and use it to get better outcomes for themselves.” Google’s Zaraisky said: “[At] Google when we make an assessment on a user – particularly financing for ads, how much we’re going to give them to start – data can really help us build that picture of potentially opening up… a higher limit to start with.” According to Zaraisky, 60% of its customers are SMEs, many of which are “not a known brand name”. However, she said that Open Banking data can help to “build that full picture of the user that we have and make sure we can best serve their needs”. Hossack said that cashflow, paying employees and suppliers, raising invoices, and “actually being paid yourself” are among the daily stresses and concerns for business owners and are all “time-consuming” administrative tasks. She continued: “So, if we start with the challenges around how do we help businesses get paid faster or make payments faster, as an example, even understanding where they stand as a business, understanding the information that they’ve got – how accurate is that? Can they make good decisions because of that? Are they working with an advisor who can help and support them make that decision? “All of those are the challenges that they’re experiencing and the ways that Open Banking can help.” Speed and UX in payments The panel went on to talk about payments and payment initiation, and to consider how new methods of paying will make a difference to SMEs and their customers. Zaraisky said: “A lot of times what we see when we’re working across any payment method is the number of screens can increase exponentially and, therefore for an SME, if you can bring this [the payment] into their product, you have a customer there that has a willingness to pay. “I’ve been through [payment] flows where I’ve clicked three times – ‘yes, I want to pay. I want to pay’ – and I haven’t actually quite got to the payment. “The chances I come back could be very low. But if you’ve brought it all into one place, that UX improvement could be quite a game changer and just making sure they capture the sale as well.” Zaraisky added: “So, I think both speed and UX improvements are potentially where Open Banking payments can really help out for SMEs.” Green suggested that, up until now, much of the focus has been on consumer-to-business payments. “For that, single payments works, and it works for business-to-business as well. But there are other optional APIs that are out there. For example, you can do file payments, or we call them bulk payments. You could use that to pay invoices, you could use that to pay payroll, depending on how many employees you have,” she added. “The really good news is that we’ve been talking to some banks about these APIs and they’ve made a commitment that they’re going to be looking at improving them in the next cycle of development that they do.” Hossack spoke about the issue of late payments in the UK, citing the statistic that SMEs are owed, on average, £22,000 in late payments and that every quarter in 2022, 52% of SMEs suffered from late payments. “Understanding why late payments happen, who is responsible for it or who is more likely to be responsible for it, is important because there are a number of different factors that clearly are at play here,” she told attendees, adding that Open Banking has the “potential” to significantly improve the situation. Share

Yapily Frequently Asked Questions (FAQ)

When was Yapily founded?

Yapily was founded in 2017.

Where is Yapily's headquarters?

Yapily's headquarters is located at 86-90 Paul Street, London.

What is Yapily's latest funding round?

Yapily's latest funding round is Incubator/Accelerator - II.

How much did Yapily raise?

Yapily raised a total of $69.4M.

Who are the investors of Yapily?

Investors of Yapily include Tech Nation Future Fifty, HV Capital, Lakestar, Sapphire Ventures, Latitude and 8 more.

Who are Yapily's competitors?

Competitors of Yapily include TrueLayer, Finix, Bud, Railsr, Bond and 7 more.

What products does Yapily offer?

Yapily's products include Payments and 4 more.

Who are Yapily's customers?

Customers of Yapily include Intuit Quickbooks, Juni and Yonder.

Loading...

Compare Yapily to Competitors

Fabrick is a open finance platform. The company offers payment solutions that enable and foster a fruitful exchange between players that discover, collaborate, and create solutions for end customers. Fabrick was founded in 2018 and is based in Biella, Italy.

Plaid operates as a technology company that focuses on providing a data network for fintech solutions. The company offers a suite of products that enable secure and easy connection of financial accounts to various applications and services. Plaid primarily serves the financial technology industry, including personal finance, lending, and wealth management sectors. Plaid was formerly known as Plaid Technologies. It was founded in 2013 and is based in San Francisco, California.

TrueLayer is an open banking platform that specializes in the financial services industry. The company offers a suite of products that enable instant bank payments, fast and verified payouts, streamlined user onboarding, and variable recurring payments, all designed to facilitate safer and more efficient financial transactions. TrueLayer primarily serves sectors such as e-commerce, gaming, financial services, travel, and cryptocurrency markets. TrueLayer was formerly known as Finport. It was founded in 2016 and is based in London, United Kingdom.

Railsr is a global embedded finance platform that operates within the financial services sector. The company provides financial services, including digital wallets, payment processing, and card issuance, all facilitated through API integration. Railsr's platform is designed to integrate into a brand's digital journey, offering rewards programs, loyalty points, and various types of cards. Railsr was formerly known as Railsbank. It was founded in 2016 and is based in London, United Kingdom.

Leveris has developed an end-to-end platform to allow financial institutions and fintech startups such as digital-only banks or challenger banks to run their services.

Teller is a company that focuses on providing API solutions for bank accounts in the financial technology sector. Their main service involves offering an easy-to-use API that allows users to connect their bank accounts to applications, enabling account verification, money transfers, payments, and transaction viewing. The company primarily serves the financial technology industry. It was founded in 2014 and is based in London, England.

Loading...