CVCs show heightened interest in early-stage rounds, even as CVC dealmaking falls to its lowest level since 2018.

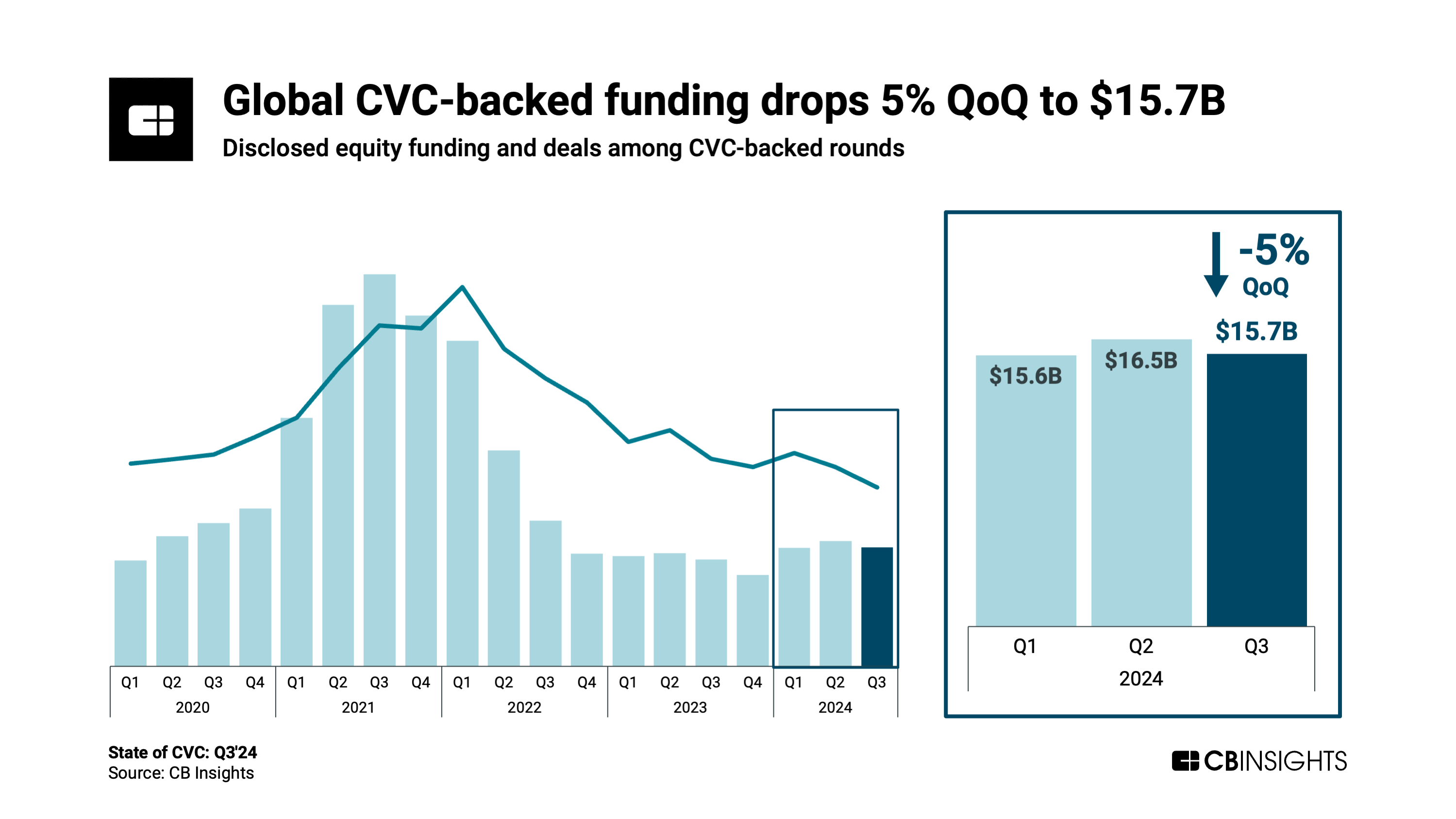

In Q3’24, global CVC-backed funding fell 5% quarter-over-quarter (QoQ) to $15.7B — alongside a 10% decline in deals — as investors navigated persistent macroeconomic headwinds from global inflation pressures and elevated interest rates to China’s economic challenges.

Despite these declines, $100M+ mega-rounds comprised 51% of total CVC-backed funding in Q3’24, a notable increase from a quarterly average of 37% in 2023. Meanwhile, two-thirds of CVC deals this year have gone to early-stage companies, highlighting a strategic shift toward more emerging opportunities, especially in AI.

Based on our deep dive in the full report, here is the TL;DR on the state of CVC:

- Global CVC-backed funding drops 5% to $15.7B in Q3’24. Nevertheless, that figure is still the second-highest quarterly level since the beginning of 2023. Meanwhile, a 10% QoQ decline to 773 deals — the lowest total since 2018 — suggests that CVCs are increasingly selective, similar to the wider venture market.

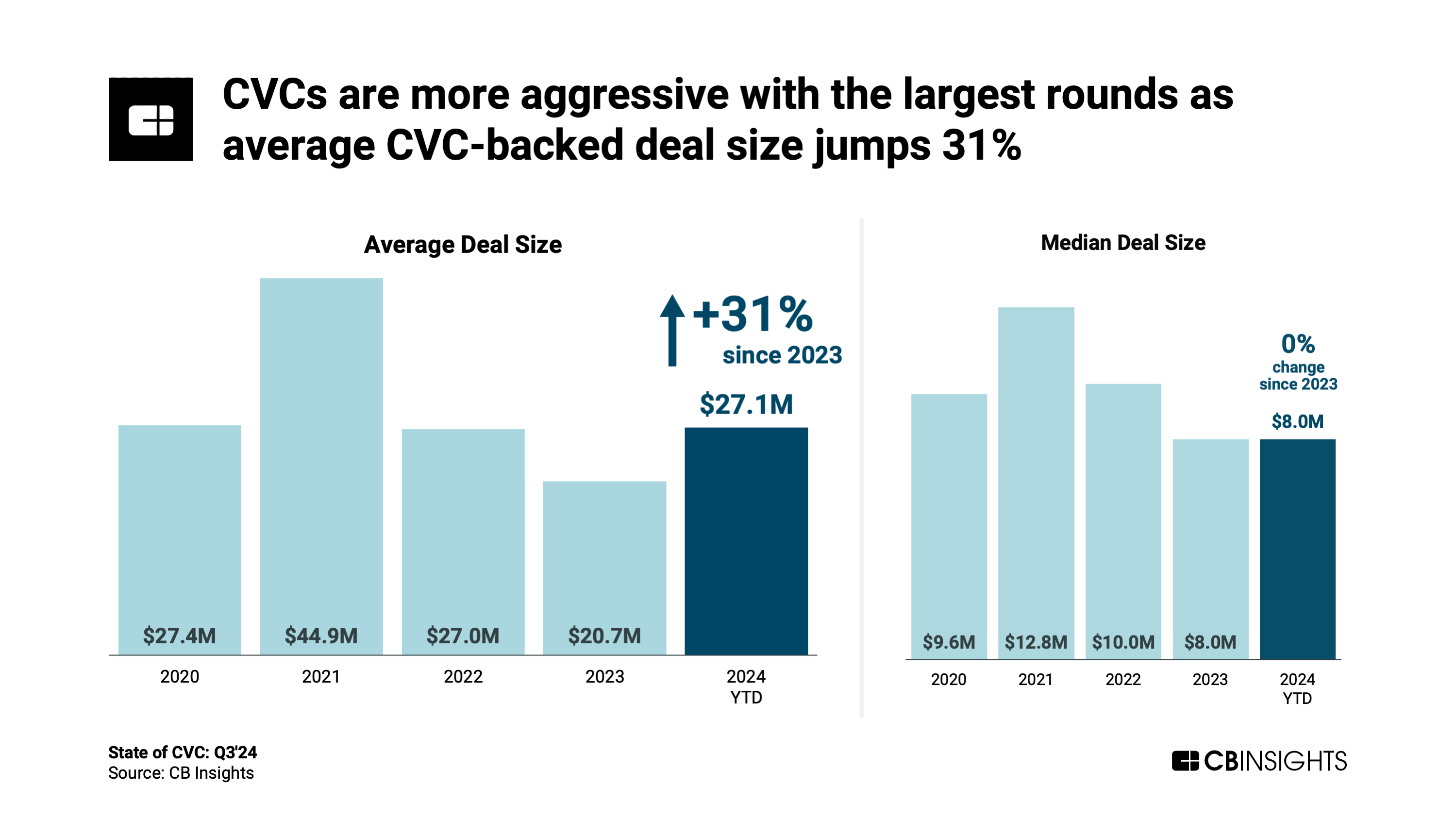

- The average CVC-backed deal size has increased 31% so far this year to $27.1M, highlighting investors’ willingness to take risks when they find the right opportunity. However, the median deal size remains the same as last year at $8M, signaling that investors are only more aggressive regarding the largest deals.

- Funding to CVC-backed mega-rounds (deals worth $100M+) represents 51% of total funding in Q3’24. This percentage — roughly in line with the first 2 quarters of 2024 — is up significantly from an average of 37% in 2023, further suggesting that investors are currently willing to make large bets when they decide to invest.

- Early-stage rounds represent 66% of total CVC deal share this year, the highest level in over a decade. CVCs are increasingly focused on early-stage startups, likely driven by the record levels of AI funding and the fact that, across investor types, 72% of deals to AI companies this year are early-stage.

- CVC-backed funding in the US ticks up to $10.5B. Among major global regions, the US continued to lead in CVC-backed funding in Q3’24, followed by Europe at $2.6B and Asia at $1.3B. Within the US, defense tech provider Anduril raised the largest CVC-backed deal with its $1.5B Series F round (CVC investors include Franklin Venture Partners), followed by AI chip developer Groq with its $640M Series D round (backed by Samsung Catalyst).

MORE VENTURE RESEARCH FROM CB INSIGHTS

- State of CVC Q2’24 Report

- State of Venture Q3’24 Report

- State of Fintech Q3’24 Report

- State of Digital Health Q3’24 Report