AI startups grab 1 in 3 VC dollars. Silicon Valley is becoming even more dominant. Positive signs from tech IPOs. We break down key changes in the venture landscape.

AI has established a commanding presence across the VC landscape.

In some ways venture has become less dramatic. The period of steep decline in funding that followed the dizzying heights of 2021 has given way to relatively moderate quarterly variations.

But even in a more sober fundraising environment, excitement over AI has become a major driving force for investors. One in every 3 VC dollars now goes to the tech. Silicon Valley, a major AI hub, is tightening its hold on investor cash. AI startups are exiting years faster than those working on other technologies.

As interest rates fall and the appetite for riskier assets increases, expect AI startups to be top of mind for an increasing number of investors in the months ahead.

Download the full report to access comprehensive data and charts on the evolving state of VC across sectors, geographies, and more.

Below, we cover key shifts in the landscape, including:

- Quarterly declines in global VC funding and deals

- AI startups grab 1 in 3 VC dollars

- Performance from recent tech IPOs

- Silicon Valley is only getting stronger

- New unicorns remain rare

- The US claims the bulk of AI innovation

- How global VC stacks up against economic output

- 76% of top deals go to B2B startups

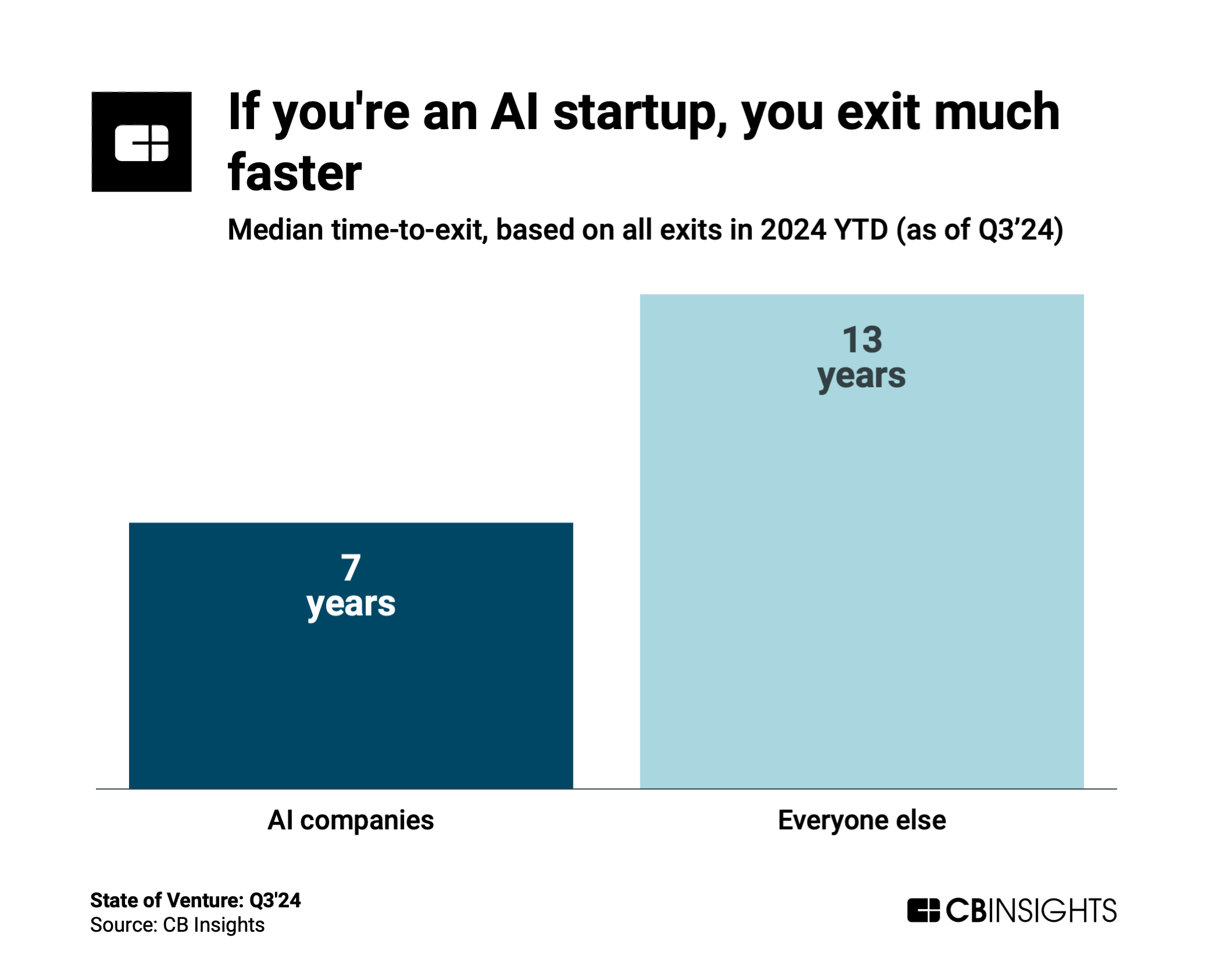

- AI startups exit 6 years sooner than the rest of tech

Let’s dive in.

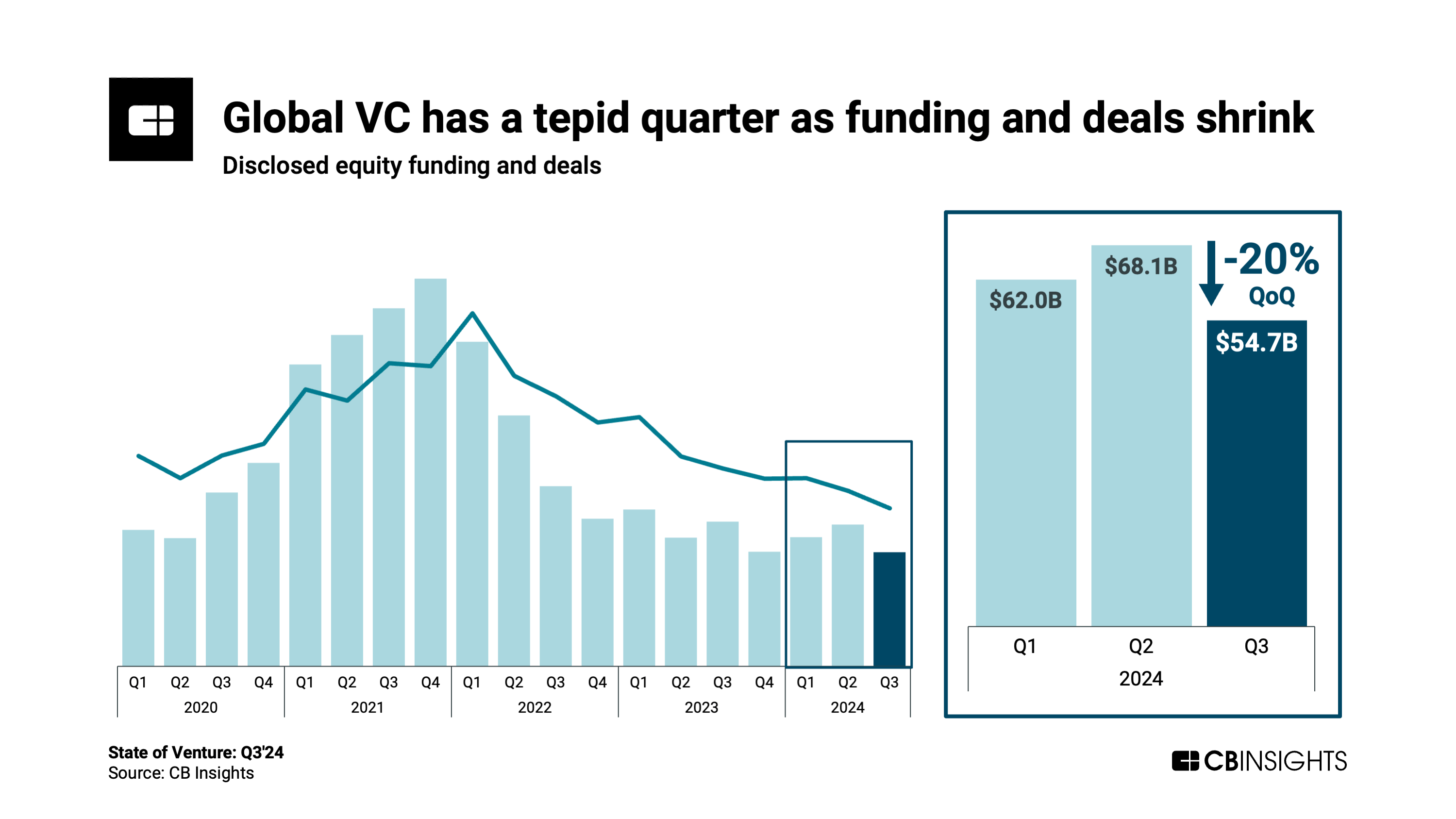

Topline figures paint a sobering picture for venture, as both global funding and deals ticked down quarter-over-quarter (QoQ). The quarterly levels place Q3’24 on par with where VC was in 2016/2017.

However, while deal volume has progressively declined, the size of deals that do happen has grown. In 2024 so far, the average deal clocks in at $13.9M (up from $12M in full-year 2023), while the median is worth $3M (up from 2023’s $2.5M).

The more cautious investment environment is likely driving a flight to quality as selective investors isolate the most promising ventures.

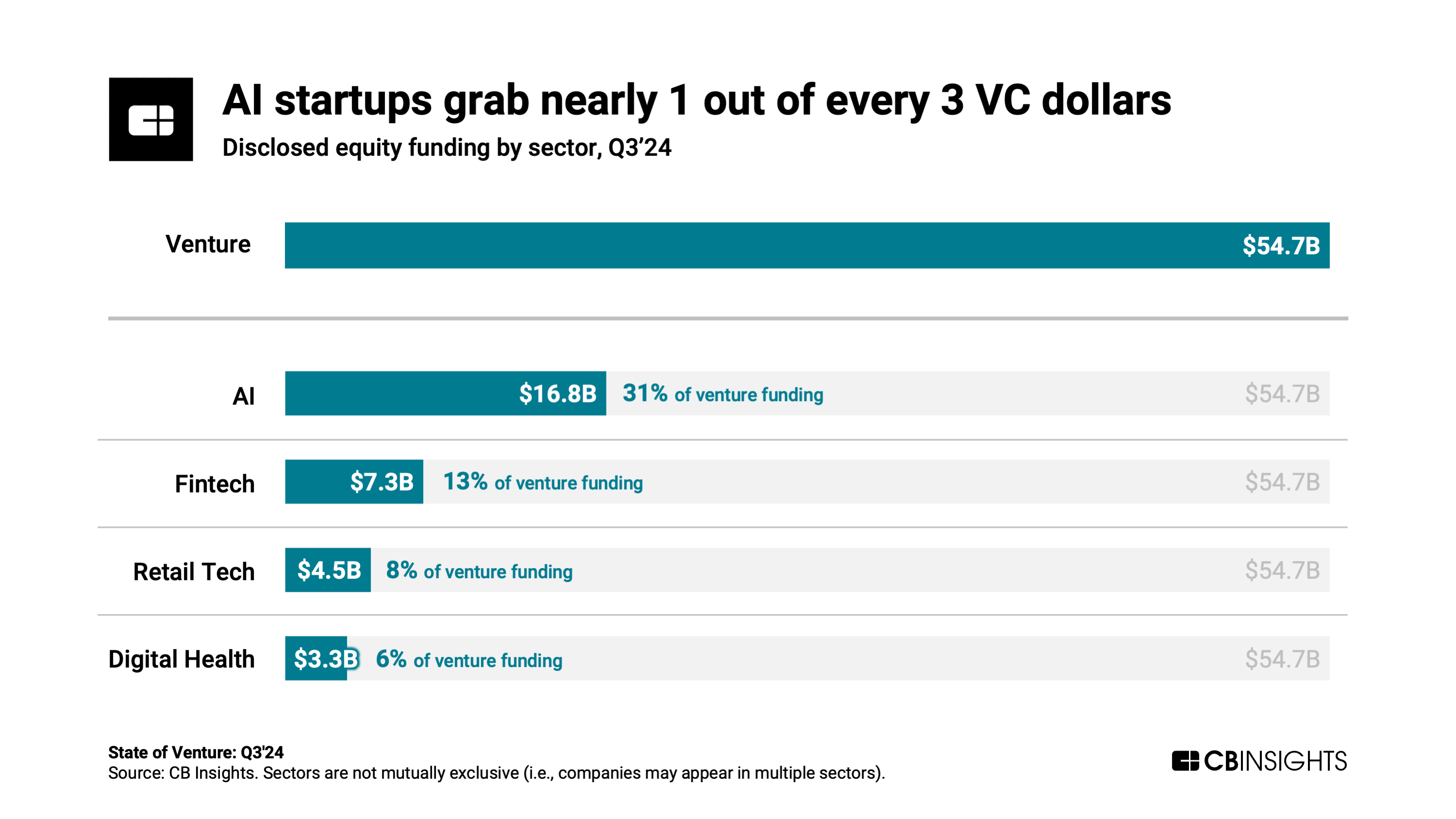

AI startups are capturing nearly a third (31%) of all venture funding right now — the second-highest share on record, following Q2’s 35%.

Within AI, a company’s age and stage don’t always correlate to the size of financing rounds. One of the largest rounds in Q3’24, for instance, was a mammoth $1B deal to Safe Superintelligence (SSI) — an early-stage startup founded in June by OpenAI co-founder Ilya Sutskever. The company has just 10 employees.

SSI’s deal is the 9th $1B+ AI equity round this year. Given their willingness to participate in such large rounds to so many companies, investors appear confident that a new tech giant will emerge from the space — and apparently have FOMO.

Yet despite investors’ bullishness, many of today’s fledgling AI startups will struggle to live up to lofty expectations, and some will ultimately fail. Even AI giants like OpenAI face the daunting task of keeping costs in control: the AI leader’s losses are expected to amount to $5B this year.

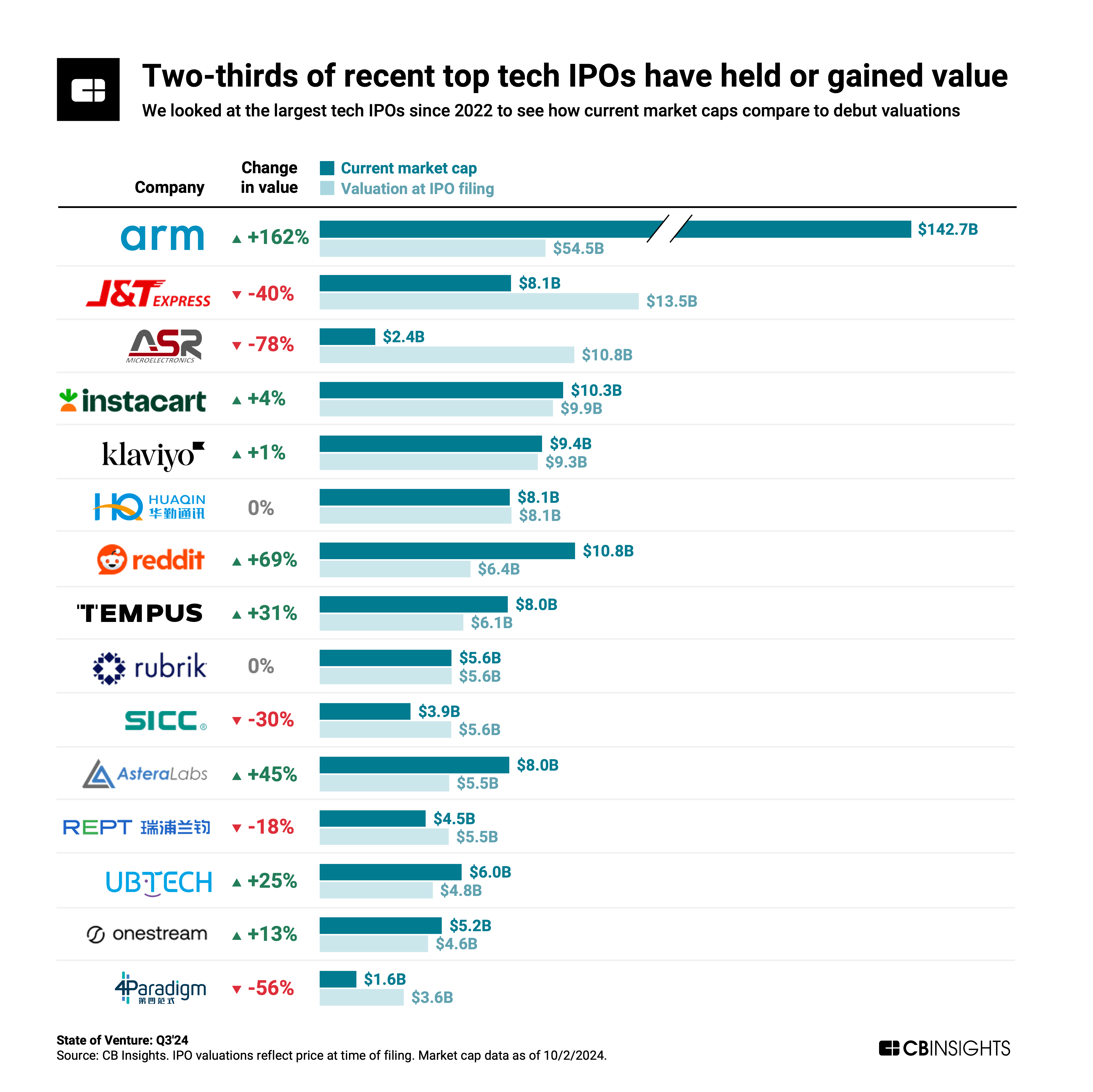

The AI boom is also giving recent public debuts a boost.

We analyzed 15 of the companies with the largest tech IPOs since 2022 to see whether they’ve gained or lost value since they filed to go public IPOs. The majority (10 out of 15) have either held steady or gained value as public players — a positive indicator for tech IPOs more broadly, which until recently were getting beaten down badly in the public markets. The fact that startups are able to maintain and even gain value as public companies will likely draw out other IPO-ready companies.

And AI is an important factor driving gains for several of these companies. For instance:

- Arm’s value has nearly tripled since it debuted late last year. The chip designer is a leader in CPUs for AI computing hardware, including providing the architecture for AI chip firms like Nvidia.

- Tempus is deploying AI across its precision medicine offerings, which has helped buoy its value by 31% since its IPO filing. (It legally changed its name from Tempus Labs to Tempus AI in early 2023.)

- Like Arm, Astera Labs, which offers AI infrastructure & connectivity hardware, has benefited from the swell in widespread adoption of AI. Its value has grown 45% since filing in March 2024.

It’s not universal — enterprise AI firm 4Paradigm, for instance, has seen its value slashed by over half since debuting. But this could be due more to geopolitical forces, as China-based 4Paradigm has faced an uphill battle in sustaining investor interest because of US restrictions. (4Paradigm was placed on a US export control list in early 2023.)

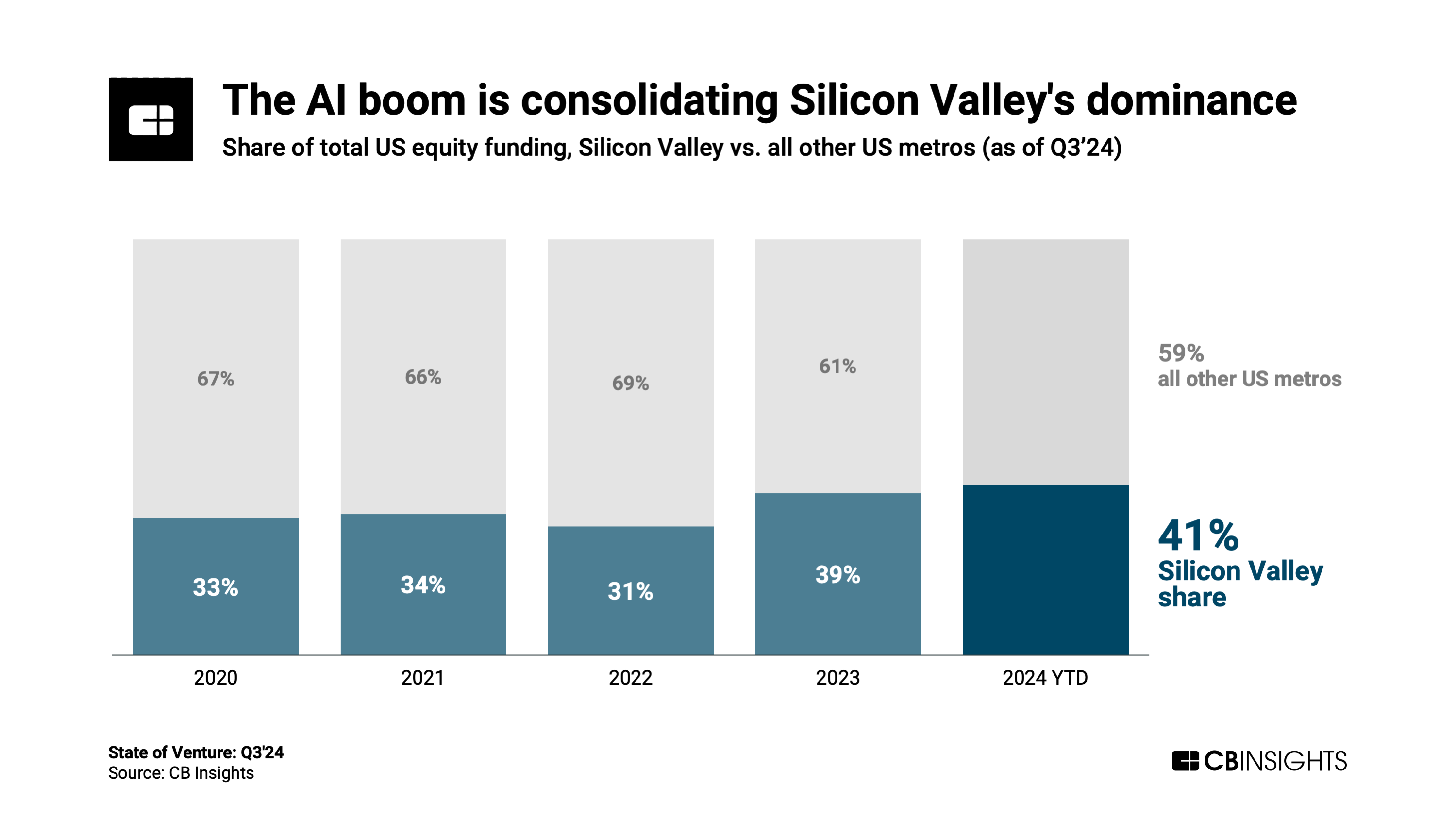

Another result of the AI explosion: Cash is concentrating in Silicon Valley, home to over a third of the US-based AI startups. In fact, the metro’s share of US venture funding — across sectors — has climbed to a recent high of 41% this year.

In Q3’24, Silicon Valley-based startups raised $10.5B — more than 2.5x that of New York ($3.9B), the second-ranked metro. LA and Boston follow, with $2.9B and $2.8B, respectively.

Notably, deal activity in Silicon Valley remains overwhelmingly early-stage — meaning it’s not just a handful of more established startups raising massive rounds. More than two-thirds of Silicon Valley’s deals this year are at the seed or Series A stages.

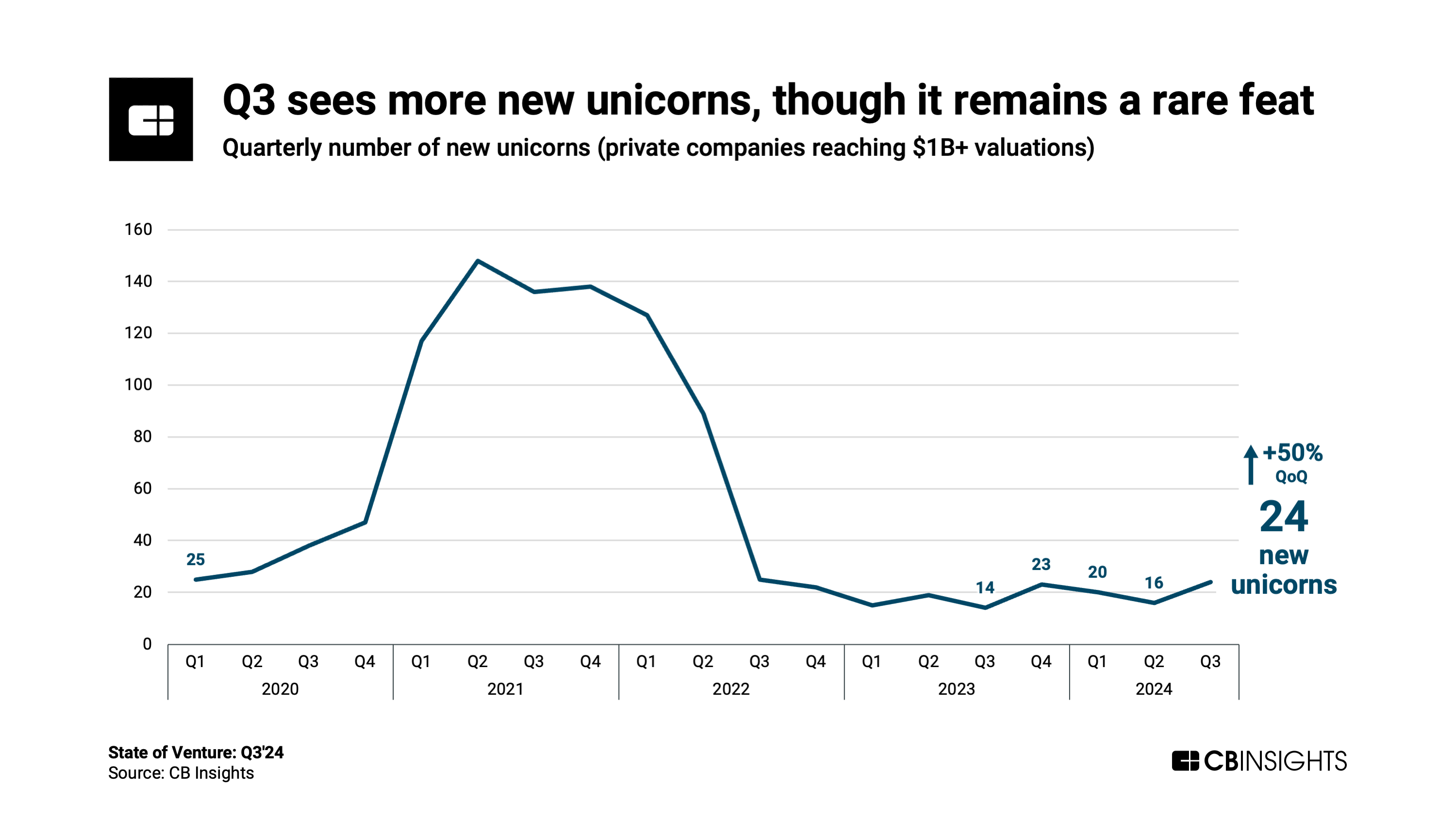

Newly minted billion-dollar startups remain few and far between. Q3’24 saw 24 startups reach that mark — a noticeable bump from the previous quarter’s 16, though a fraction of what we saw during the tech boom of 2021 and early 2022.

Valuations remain pressured at the later stages of investment, with many of the unicorns minted in years gone by likely worth less than $1B in reality. On the other hand, valuations are showing strength at the earlier stages. Among seed-stage startups, the median valuation for deals this year is $13.5M — the highest annual level on record.

There are a few common themes among the latest batch of new unicorns:

- AI is minting more unicorns than any other sector. More than half of the new unicorns in Q3’24 are AI companies. Among these, several are working to bring greater spatial awareness to AI systems, from Skild AI’s intelligent humanoid robotics to World Labs’ 3D world-building tools. Others are developing enterprise AI agents & copilots, like Harvey in the legal domain and Codeium in software engineering.

- India’s startups are climbing the ranks. The country contributed 3 of Q3’24’s new unicorns: Ather Energy, MoneyView, and Rapido. India ranks third globally for total unicorns after the US and China, and it had a strong funding quarter in Q3’24, with startups raising $4B — up 29% QoQ and 111% YoY.

- a16z and Sequoia are the most active investors in backing new unicorns. The investors each backed 4 of Q3’24’s freshly minted $1B+ companies. Andreessen Horowitz invested in Saronic Technologies, World Labs, Story Protocol, and Safe Superintelligence; while Sequoia Capital backed Skild AI, Harvey, Chainguard, and Safe Superintelligence.

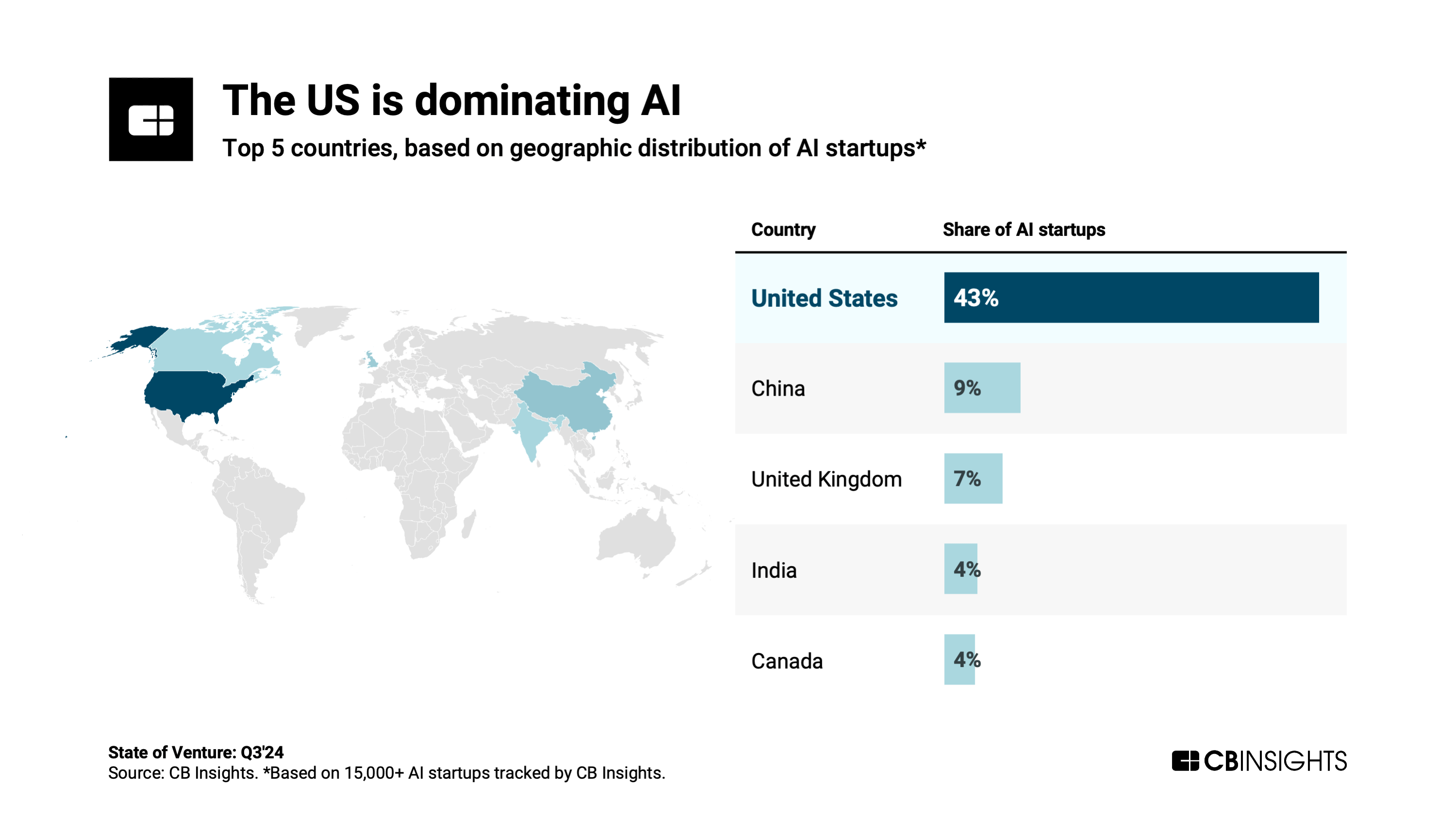

CB Insights tracks over 15,000 AI startups globally. And while 99 countries and regions around the world have at least 1 AI startup, the US is the undisputed leader in AI startup activity — and by a substantial margin.

43% of all AI startups are based in the country. The distant No. 2 and No. 3 countries are China (9% of AI startups) and the UK (7%).

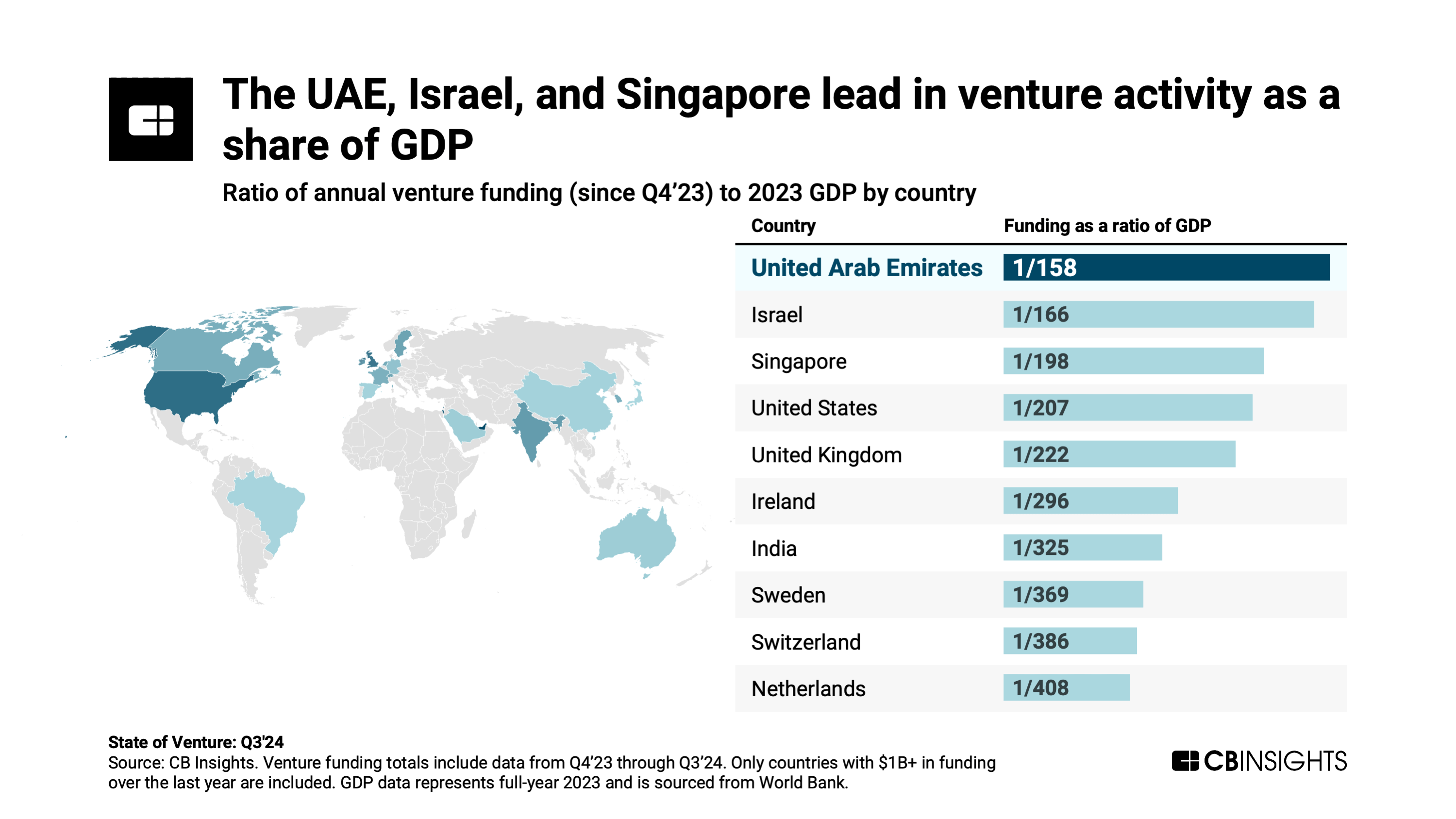

While the US has long dominated the global venture scene when it comes to absolute funding and deal activity, several countries rank above the US in terms of the ratio of venture funding to GDP: the United Arab Emirates, Israel, and Singapore.

These 3 countries pace ahead of the US in terms of VC as a proportion of overall economic activity, suggesting they are punching above their weight in terms of fostering startup activity.

For instance, UAE-based startups have raised over $3B in funding over the last year (since 10/1/2023), and the country’s 2023 GDP came in at $504B. That represents $1 in VC to $158 in GDP (1/158) — a stronger ratio than any other country with at least $1B in annual venture funding.

Activity in the region has recently been fueled by AI firm G42, which raised a $1.5B round from Microsoft in April. (As part of the deal, G42 will use Microsoft’s Azure cloud offering, and Microsoft will also gain access to G42’s data centers.)

Israel and Singapore hold the No. 2 and 3 spots, with venture funding to GDP ratios of 1/166 and 1/198, respectively.

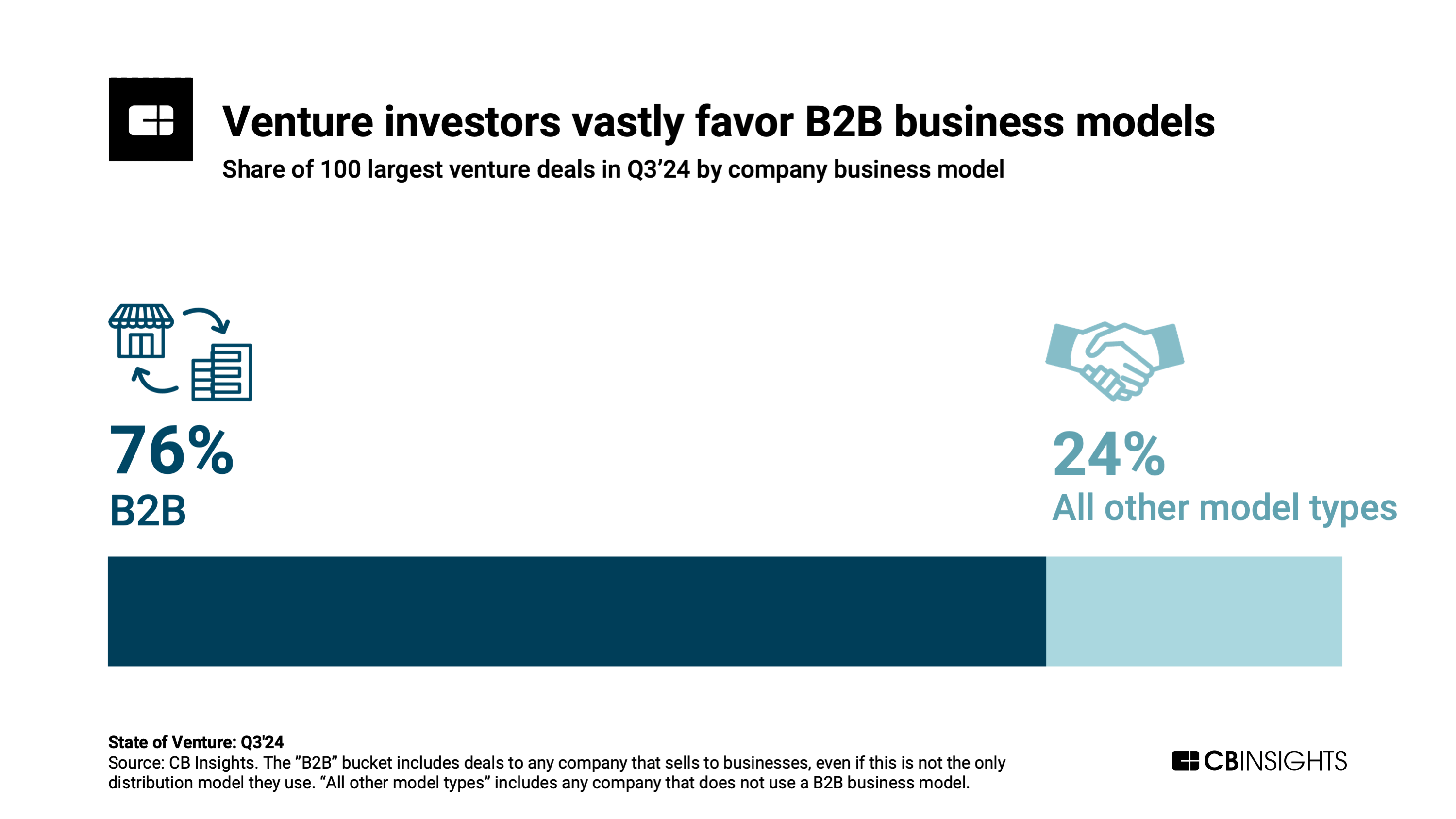

Right now, the venture capital industry is all in on B2B startups. Among the 100 largest deals in Q3’24, three-fourths went to startups that use a B2B business model (either exclusively or in combination with other models like B2C or B2G).

The B2B distribution model — particularly at the enterprise level — has gained appeal in recent years as a potentially more stable, recurring source of revenue for startups, especially during periods of volatile consumer spending.

The buzz around AI is translating to faster exit velocity for startups in the space. Breaking down all the exits that have taken place this year, it’s clear AI startups exit at a much faster rate — 6 years faster, to be exact. It takes the median AI company just 7 years to exit from the year it was founded, compared to 13 years for non-AI companies.

While this trend holds true for recent AI IPOs, it’s most commonly seen among M&A deals, which represent the vast majority of AI exits this year.

Corporations are among the top acquirers of AI startups, with many looking to gain an edge by rapidly adding novel AI tools to their product suites.

- Nvidia has acquired 3 AI startups this year: Deci and Run:ai, both in April; and OctoAI, just last week. All 3 operate at the infrastructure layer of AI development and signal Nvidia’s ambitions to expand across the AI software stack.

- Zendesk has acquired 2 customer service-focused players — Ultimate and Klaus — as it builds out its own AI agent offering to automate customer interactions.

- Salesforce has similarly pledged to go all in on AI agents. To this end, it acquired 2 AI startups last month: Tenyx and Zoomin.

Another driving factor is “acqui-hires,” where an acquirer purchases a startup primarily for its talent. We’ve seen this among some of the youngest AI startups to be acquired. For instance, SydeLabs and Laiyer, both founded in 2023, were acquired by Protect AI this year. In both cases, Protect AI absorbed the startups’ teams.

If you aren’t already a client, sign up for a free trial to learn more about our platform.